In February I turned 40, and I’ve been thinking about how much my mindset has changed in the past 10 years. Many years ago, when I was working in education, my wife and I basically lived paycheck to paycheck. We ate out all the time and had fun with our teacher friends on the weekends, usually exhausted from working 18-hour days, six days a week. We wanted to pay off student loans, and our only thought about saving for retirement was that we were paying into a pension.

After a decade as a retirement-focused financial planner in Dayton, Ohio, I’ve realized how important it is to create future flexibility. I see this play out in real time on a regular basis. Some of the families I serve share that they’re thankful they built a strong foundation of retirement savings, while others kick themselves about missed opportunities. They wish they had taken advantage of things like Health Savings Accounts or the tax-free growth of Roth IRAs.

With my wealth management clients, I always try to keep our focus on figuring out our next best step. I firmly believe that whether retirement is next year or eight years away, we can’t predict the future, but we can figure out the next baby step to give you more options and confidence. So if you’re asking yourself, “When should you start retirement planning in Ohio?” the good news is that you can take a positive step today to improve your situation.

In this article, we’ll discuss what planning looks like at different ages and some steps you can explore to orchestrate your ideal retirement.

Key Takeaways

- The Right Time to Start: Retirement saving begins with your first paycheck. But as you get closer to making the leap, your mindset will probably shift from accumulation to crafting a focused plan

- Ohio’s Savings Advantage: Lower housing costs keep Ohio’s cost of living roughly 8% to 12% below the national average. You can target a much more achievable portfolio size to fund a comfortable lifestyle here than in higher-cost states.

- Your Next Best Step: You can’t change the past or predict the future, but you can improve your retirement confidence today. No matter your age, a successful plan is built by breaking things down into small, actionable baby steps.

When Should You Start Retirement Planning in Ohio?

The timing of planning for retirement doesn’t really change just because you live in Ohio. Whether you live in Dayton or San Diego, you’ll need a strategy for the day you stop working. Retirement might be your choice, or maybe health changes or job shifts make the decision for you. A recent Gallup poll stated that the average retirement age in the United States is around 61. A lot of people plan to work until 65 or 67, but health transitions or corporate downsizings frequently pull that date forward.

The real variable when it comes to planning for retirement is your stage of life. If you’re raising a family, paying down student loans, or shifting careers, retirement planning is going to be naturally less focused than if you’re 5 years from making the leap. But there’s always something you can do to set yourself up for a more comfortable version of financial independence.

Where Ohio does make a difference in retirement planning is how much you’ll need to save. In one of my recent blog articles, I shared that the overall cost of living in Ohio is reported to be about 8% to 12% below the national average. GoBanking Rates claims that the average American retirement household spends around $57,818 per year but Ohio retirees average closer to $53,308. If you assume a 4% retirement withdrawal rate, this difference means you could retire with over $100,000 less than the average American and feel comfortable here.

For a deeper dive into the cost of living for retirees in Ohio, check out my recent article: How Much Do You Need to Retire Comfortably in Ohio? A Budget-Based Guide.

Why Starting Early Matters (Even in Ohio)

If you’re over 50 and planning your retirement, a phrase like “starting early” probably sounds like advice meant for the youngsters. But early is really a relative term. Thanks to compound interest, the adjustments you make to your savings right now might still have time to ripple forward into big benefits.

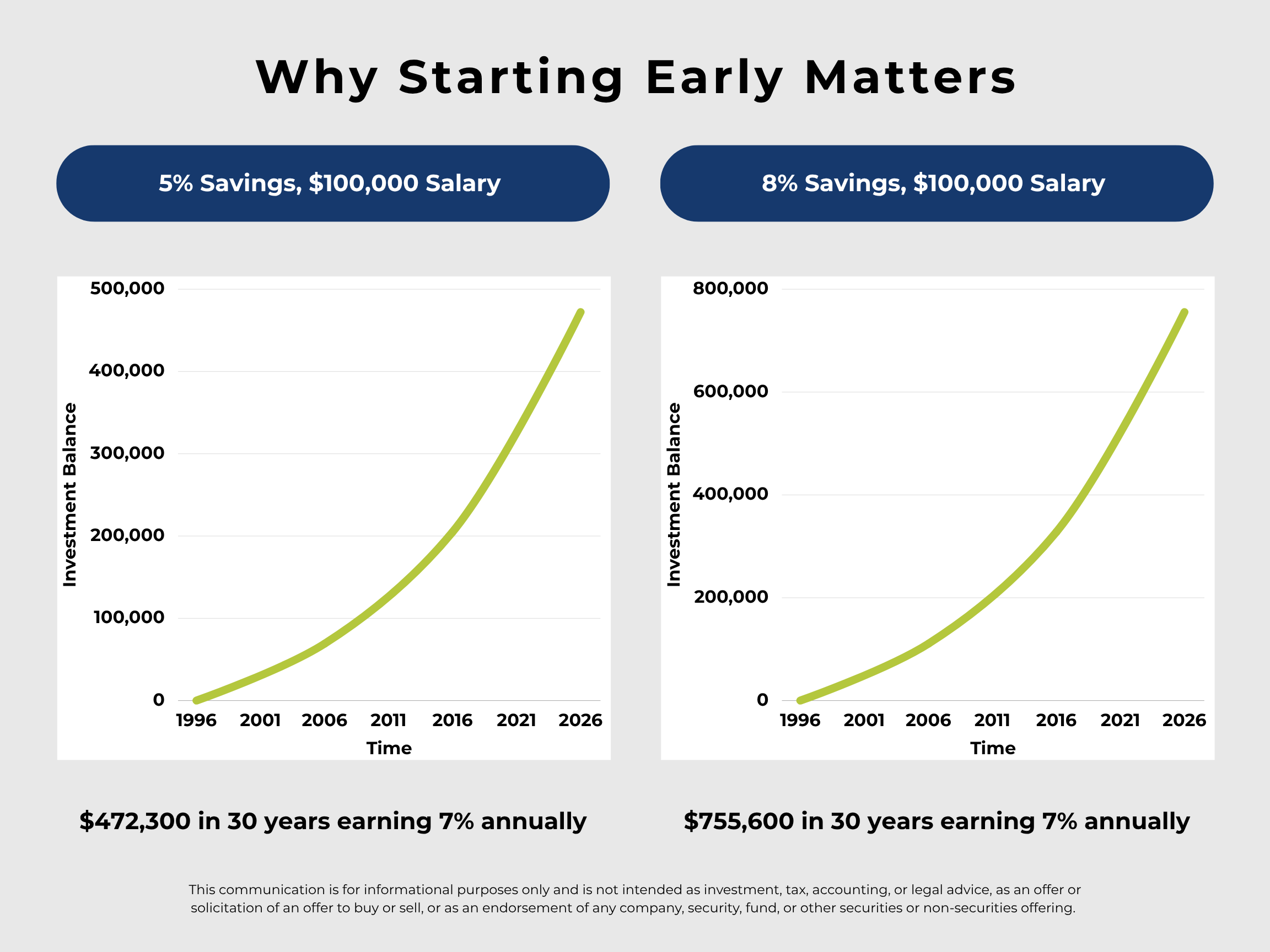

To understand why timing matters, let’s look at what happens when you maximize your company match:

On a $100,000 salary, contributing 5% to your 401(k) means you’re saving $5,000 a year. If you let that ride for 30 years at a 7% average rate of return, you might end up with around $472,300. But if you included a 3% employer match from day one, your total annual savings would have been $8,000. Over those same 30 years at 7%, that total balance might be around $755,600. You added a whopping $283,300 more for a few extra percent savings.

According to Vanguard’s 2025 How America Saves report, the average promised employer match sits even higher around 4.6%. You can’t change the past, but leaving money on the table today is the equivalent of turning down a six-figure retirement bonus.

If you’re over 60 and reading this article, I don’t want you to look at that math and feel hopeless. I remind my clients regularly that retirement prep isn’t just about accumulating big portfolios. You need time to come up with a vision for a meaningful life without your job to identify with every day. You need time to find the right health coverage, and to map out a strategy for income and taxes. The sooner you start the retirement planning process, the smoother you’ll make the transition.

Ohio Retirement Planning by Age: What to Do at Every Stage

Having built a retirement planning business named after being prepared for the next stage of life, you can probably guess that I care quite a bit about retirement readiness. And I know firsthand that planning means different things depending on what’s going on in your life. Every stage requires a different rhythm.

Here’s how to synchronize your strategy based on where you are today:

- In Your 20s-40s: Build the Foundation

- In Your 50s: Catch Up and Refine Your Strategy

- In Your 60s and Beyond: Prepare for Income and Withdrawals

In Your 20s-40s: Build the Foundation

In the first half of your career, your focus is on everything except retirement. You’re raising a family, managing your mortgage, paying off student loans, and trying to build your career. Life is packed, so you don’t need to obsess over retirement specifics. Just consider getting your financial systems running automatically and let compound interest work for you.

Some ideas here include:

- Automate savings

- Build awareness

- Minimize debt

- Expand your instruments

Automate Savings

Your biggest asset early on is time. Focus on getting started in your employer-sponsored retirement plan, and automate your savings before the money ever hits your checking account. If your employer offers a match, reference my above example and take full advantage of the free money as quickly as you can. It’s also smart to automate savings for cash goals like an emergency fund and buying a new car.

Build Awareness

You don’t have to be a budget maniac, but you should be aware of what you spend and be intentional about how you use your paycheck. Awareness means you can actually make decisions like putting money toward things that really matter, getting out of debt faster, and saving for big dreams. Also, retirement planning is a lot easier if you have a clear grasp of how much you spend.

Minimize Debt

Loans can be helpful because they let you get things you need before you have the cash. But the flip side is that you end up paying for things you wanted in the past for a long time. And the cycle can become vicious. The sooner you pay off old bills, the more cash flow you free up to save and spend on what matters now.

Expand Your Instruments

Once you’re capturing your company match, you can start looking at more advanced strategies. You could add a Health Savings Account (HSA) and invest it for long-term growth. According to Fidelity Investments, the HSA is one of the most solid wealth-building tools because of its triple tax advantage. Contributions reduce your taxable income, the balance grows tax-deferred, and withdrawals are entirely tax-free for qualified medical expenses. If your income allows, you could also save in a Roth IRA or build a brokerage account for tax-friendly early retirement savings.

In Your 50s: Catch Up and Refine Your Strategy

My clients are all over age 50. Their kids are starting to move out, their income is feeling a bit more comfortable, and retirement is starting to feel real. Your 50s is a fabulous time to hit the gas pedal on growth and savings.

In a recent blog article about Investing in Your 50s, I discussed a number of strategies to focus on, including:

- Avoid lifestyle creep

- Maximize catch-up contributions

- Stay growth-oriented

Avoid Lifestyle Creep

When you pay off your car, your mortgage, or finish helping your kids save for college, it’s tempting to upgrade your lifestyle. Shiny objects will immediately pop into view, like your friend’s brand new kitchen remodel. But your 50s are such a great window to take your newly freed-up income and divert it straight into your savings to supercharge your retirement. And you might have enough time to let compounding still work in your favor.

Maximize Catch-Up Contributions

According to IRS catch up contribution rules for 2026, you can save $24,500 and an extra $8,000 each year in your 401(k). This blossoms to an extra $11,250 between ages 60-63 thanks to the Secure Act 2.0. When you turn 50, you’re able to save $7,500 plus an extra $1,100 in an IRA or Roth IRA. And if you have an HSA, you can contribute an extra $1,000 starting at age 55.

Stay Growth-Oriented

If you’re 52 and plan to retire at 65, you still have plenty of time to build long-term wealth. Consider keeping your portfolio in growth mode until you’re getting closer to around 5-7 years from retirement.

In Your 60s and Beyond: Prepare for Income and Withdrawals

This is where things get both exciting and overwhelming as you put the pieces together. You’re getting ready to transition from being a saver with a steady paycheck to financial independence.

Tips in your 60s and beyond include:

- Get clear about retirement

- Plan your income and benefits

- Arrange your investments

- Plan for healthcare

- Update your estate plan

Get Clear About Retirement

Ask yourself what a typical day, week, and month will actually look like, and who you’ll socialize with once you stop seeing coworkers every day. When your job title disappears, who will you be? What will feel meaningful when you have the freedom to spend your time anyway you want? How will you stay healthy and mentally strong?

Plan Your Income and Benefits

The closer you get to retirement, the more important it is to map out a clear plan for income. You’ll need to figure out how much you can sustainably withdraw and the right order based on your investment accounts. Social Security and pension timing are a big part of this work. Income planning can be complex, so I highly suggest speaking to a professional if it feels overwhelming.

Arrange Your Investments

Your asset allocation should always be driven by your time horizon (when you’ll need to spend your savings). This doesn’t mean you stop growing your money in your 60s, but it does mean you need to build a plan for income in down markets. You’ll probably want to build a buffer of bonds and cash to fund your income without having to sell stocks at a loss. Most of my retiree clients have built a buffer of at least 3-10 years worth of their retirement income in conservative assets inside their accounts.

Plan for Healthcare

If you plan to stop working before age 65, you’ll be responsible for finding health coverage via COBRA or the ACA Marketplace until Medicare kicks in. When you turn 65, Medicare comes with strict enrollment timelines and hidden costs like IRMAA premiums based on your past tax returns. To learn more about this topic, check out my recent article on Planning for Health Insurance in Retirement.

Update Your Estate Plan

Retirement prep goes beyond generating a predictable monthly paycheck. You’ll need to take some time to review your Will or Revocable Living Trust so that your spouse and family are protected. You’ll want to make sure your financial and healthcare Powers of Attorney are up to date in case you become incapacitated.

Retirement Planning Considerations in Ohio

Here are some important things to consider when you build your retirement plan as an Ohio resident:

- Cost of Living: Ohio’s overall cost of living is reported to be roughly 8% to 12% below the national average, driven thanks to our affordable housing costs. Recent Zillow data shows that the median home sale price in Ohio sits at approximately $216,833, compared to a national median of $398,000.

- Income Taxes: Starting in 2026, Ohio is moving to a flat income tax rate of 2.75% for taxable income over $26,050. Also, as a retiree here, our state does not tax your Social Security retirement benefits. Be sure to check out my article, Ohio Tax Retirement Strategies if you want to learn more.

- Estate and Inheritance Taxes: According to the Ohio Department of Taxation, the state’s estate tax was fully repealed on January 1, 2013. This means Ohio doesn’t impose any additional inheritance tax burdens on your family. Federal estate tax rules do still apply.

- Healthcare Costs: Ohio offers world-class medical networks like the Cleveland Clinic, but healthcare is still a major expense. Research by Fidelity Investments finds that the average 65 year old couple could expect to pay $345,000 after-tax on healthcare over the course of retirement.

How Much Should You Be Saving for Retirement?

I wish there was a magic formula but the answer really depends on how much time you have to save, how much income you have, and what you want your retirement income to look like.

To give you an idea of how this might vary over the course of your life, let’s look at an example. A married Ohio couple wants to retire at age 65 with a gross annual retirement income of $100,000.

Assuming they receive $50,000 a year in combined Social Security benefits, their portfolio needs to generate the remaining $50,000. By leaning on a realistic initial withdrawal rate between 4.6% to 5.3%, they need a total household portfolio around $1 million.

If their investments average 7%, the following chart shows the different savings percentages they’d need to use depending on when they started saving:

| Starting Age | Years to Save | Total Household Savings | % of Joint Income |

| Age 20 | 45 | $292 monthly | 3.5% |

| Age 30 | 35 | $603 monthly | 7.2% |

| Age 40 | 25 | $1,318 monthly | 15.8% |

| Age 50 | 15 | $3,316 monthly | 39.8% |

| Age 60 | 5 | Not Possible | Not Possible |

*Assumes $0 starting balance, 7% return, and a $100,000 combined pre-retirement income.

While starting from absolute scratch in your 50s or 60s hits obvious financial and legal IRS limits, the reality is that you probably aren’t starting from zero. By the time you hit the peak of your career, you’ve probably accumulated something in your 401(k), built up some home equity, and your employer matching contributions are helping with the heavy lifting.

What If You’re Starting Late?

If you feel like you’re a bit behind schedule, you can still orchestrate a successful retirement by:

- Maximizing catch up contributions to accounts like your 401(k), 403(b), 457, TSP, IRA, Roth IRA, and HSA.

- Explore downsizing your home to lower your expenses. Ohio’s housing market is ideal for this.

- Possibly work past your full retirement age to maximize your Social Security retirement benefits and give you more time to save.

- Reduce your spending if you feel your retirement accounts won’t be able to sustain enough income.

- Get help from a professional. As a fee-only retirement planner, I’m a bit biased but having expert advice from a neutral party is a great way to remove emotion from your decision making.

Common Retirement Planning Mistakes to Avoid

These are some common and costly missteps I see savers make in Dayton, Ohio on a regular basis:

- Not Having Enough Cash: Failing to build a large enough cash to absorb irregular retirement expenses like home repairs or vacations. This usually means extra, draining retirement withdrawals or credit card debt.

- Over-Concentration into One Sector: Allocating an employer’s retirement plan heavily into a single fund like the S&P 500 just because the returns look good. This builds an unintended layer of risk for retirement timing if that sector performs poorly.

- Not Understanding IRMAA: Taking large account withdrawals that spike reported household income. These can trigger higher taxes and Medicare premium surcharges that can’t be appealed.

- Buying Cars with High Interest Rates: Financing vehicles at high rates without building a structured plan ahead of time to save up and pay cash. Car values depreciate quickly and debt makes spending in retirement feel tight.

- Doing Roth Conversions Blindly: Attempting to convert pre-tax retirement accounts to Roth without the active help of a tax professional. I’ve seen this lead to higher taxes, underpayment penalties, and Medicare surcharges.

- Doing What a Neighbor Did: Making major financial and investment decisions simply because a neighbor or coworker did. Maybe it worked for the neighbor, but it might not be the right strategy for everyone.

- Claiming Social Security Early Out of Fear: Rushing to claim benefits before someone’s full retirement age out of worries that Social Security will run out. This can lead to earnings penalties for going back to work and a smaller lifetime benefit check.

- Taking No Survivor on a Pension: Opting for a single-life pension payout to get the highest monthly check without running the math. I’ve seen this leave spouses in a bad spot later in retirement, especially if there isn’t a solid insurance plan.

Want One-on-One Guidance? Contact Stage Ready Financial Planning Today for a Complimentary No-Commitment Consultation

Stage Ready Financial Planning specializes in helping Ohioans over 50 orchestrate their ideal retirement with confidence. Whether you’ve saved $750,000 or $2 million, the transition is complicated and overwhelming. I don’t just “do the math.” I bring the discipline of an educator and conductor to your portfolio, helping you synchronize your investments, tax strategy, and retirement benefits into one cohesive retirement plan.

Let’s make sure your plan is performing at its peak so you can enjoy the music of a retirement well lived. Schedule your intro call today!

Frequently Asked Questions (FAQs)

When should I start retirement planning if I live in Ohio?

Technically retirement planning begins with your very first paycheck, but the type of planning you focus on will change as you get older. In your 20s through 40s, you’ll probably focus on maintaining a healthy savings tempo and maximizing employer matching contributions. In your 50s and 60s, your mindset might shift from basic asset accumulation to preparing for a realistic retirement. You’ll start getting clear about your goals for retirement, maximize catch-up contributions, and map out your plan for healthcare and income.

How much do you need to retire comfortably in Ohio?

This might sound frustrating but there’s really no magic number. Your personal target for comfort depends entirely on your rhythm of spending. Shop regularly at Whole Foods, Amazon, and love to travel? Then maybe your number will be pretty high. Buy all your groceries at Kroger and Walmart and never go out to eat? The opposite might be true. Ohio’s cost of living is reported at roughly 8% to 12% below the national average, so your savings can stretch further here than some other states. But rather than relying on rules of thumb, you can map out your own target by checking out my step-by-step guide on How Much Is Needed to Retire in Ohio.

Are there tax breaks for retirees in Ohio?

Yes, Ohio is relatively tax-friendly for retirees. The state does not tax your Social Security retirement benefits. Also as of 2026, Ohio has transitioned to a flat state income tax rate of 2.75% for taxable income over $26,050. For residents aged 65 or older with a modified adjusted gross income under $100,000, the state provides tax breaks like the Senior Citizen Credit. There is also the property tax Homestead Exemption for low-to-moderate-income seniors. To learn more about taxes for Ohio retirees, take a look at my recent article on Ohio Tax Retirement Strategies.

Can I retire early in Ohio on a moderate income?

This depends on what you consider moderate income and the age you consider “early.” That said, achieving an early retirement in Ohio is possible thanks to our highly affordable real estate market. If early retirement for you is sometime in your 50s or early 60s, you’ll need to pad your retirement income to pay for pre-Medicare health insurance and you won’t have Social Security benefits yet. You’ll need to be strategic to avoid early withdrawal penalties for your retirement accounts before you turn 59.5. And because you’ll be living on your own savings longer, you’ll need to build a sizable portfolio that can last as long as you do.

Author Bio

Joseph A. Eck, CFP®, is the owner and lead financial advisor at Stage Ready Financial Planning. He’s dedicated to helping retirement savers like you achieve peace of mind by orchestrating a retirement plan that accounts for all of life’s transitions. Whether you’re trying to maximize retirement savings or navigating the timing of Social Security, Joe provides down-to-earth guidance to help you improve your financial future. As a former educator and a retirement planner for over a decade in Dayton, he brings a conductor’s precision to the complexity of your portfolio. Click here to learn more about Joe.

About Stage Ready Financial Planning

Stage Ready Financial Planning helps retirees and savers over 50 throughout Dayton and Southwest Ohio stay in sync with their goals through fee-only financial planning and fiduciary wealth management. Designed for households with $750,000+ invested for retirement, Joseph Eck, CFP® helps clients coordinate retirement income, investments, taxes, and more into one cohesive strategy.

From orchestrating predictable retirement income to reducing unnecessary taxes and market “noise,” Stage Ready Financial Planning was built to help clients enjoy retirement with clarity, confidence, and financial harmony.

Article References

- GOBankingRates. “6 Reasons You Need at Least $635K (Plus Social Security) To Retire in Ohio.” Accessed June 1, 2026. https://www.nasdaq.com/articles/6-reasons-you-need-least-635k-plus-social-security-retire-ohio

- Gallup. “Nonretirees’ Worry Remains High: Actual vs. Expected Retirement Age Trends.” Gallup News, May 6, 2026. URL: https://news.gallup.com/poll/709319/nonretirees-worry-remains-high.aspx

- Vanguard. “How America Saves 2025: Key trends and insights.” Accessed June 1, 2026. https://corporate.vanguard.com/content/corporatesite/us/en/corp/articles/how-america-saves-2025-key-trends-insights.html

- Fidelity Investments. “HSA contribution limits and eligibility rules.” Accessed June 1, 2026. https://www.fidelity.com/learning-center/smart-money/hsa-contribution-limits

- IRS. “401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500.” Accessed June 1, 2026. https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500

- Fidelity Investments. “Prepare for health care in retirement.” Accessed June 1, 2026. https://www.fidelity.com/learning-center/wealth-management-insights/how-to-prepare-for-health-care-costs-in-retirement

This communication is for informational purposes only and is not intended as investment, tax, accounting, or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision. Past performance is no indication of future results.