If you’re close to or in retirement and wondering, “do I need a trust or a will?” you aren’t alone. You’ve known for a long time that you need an estate plan, but it’s easy to get overwhelmed by confusing terminology and legal jargon. Estate planning confusion is so common that, according to a 2026 study by Trust & Will, 56% of U.S. adults have no estate documents.

This article will break down the difference between a will and a trust. As a fee-only financial advisor, I’ll dive into the estate planning basics you need to know to make sure you have the right documents in place to protect your family.

Key Takeaways

- Privacy and Speed: A will becomes public record and can take a year to clear probate, whereas a trust stays private and allows your loved ones to access accounts in weeks.

- Pour-Over Safety Net: Most successful estate plans don’t choose between a will or a trust; they use both including a “pour-over will” to move any forgotten assets into the trust.

- Tax Efficiency: Leaving pre-tax retirement accounts like an IRA to your estate through a will can trigger the top 37% tax rate in 2026 after just $16,250 of income. Beneficiary designations or a trust can create a more tax-friendly distribution.

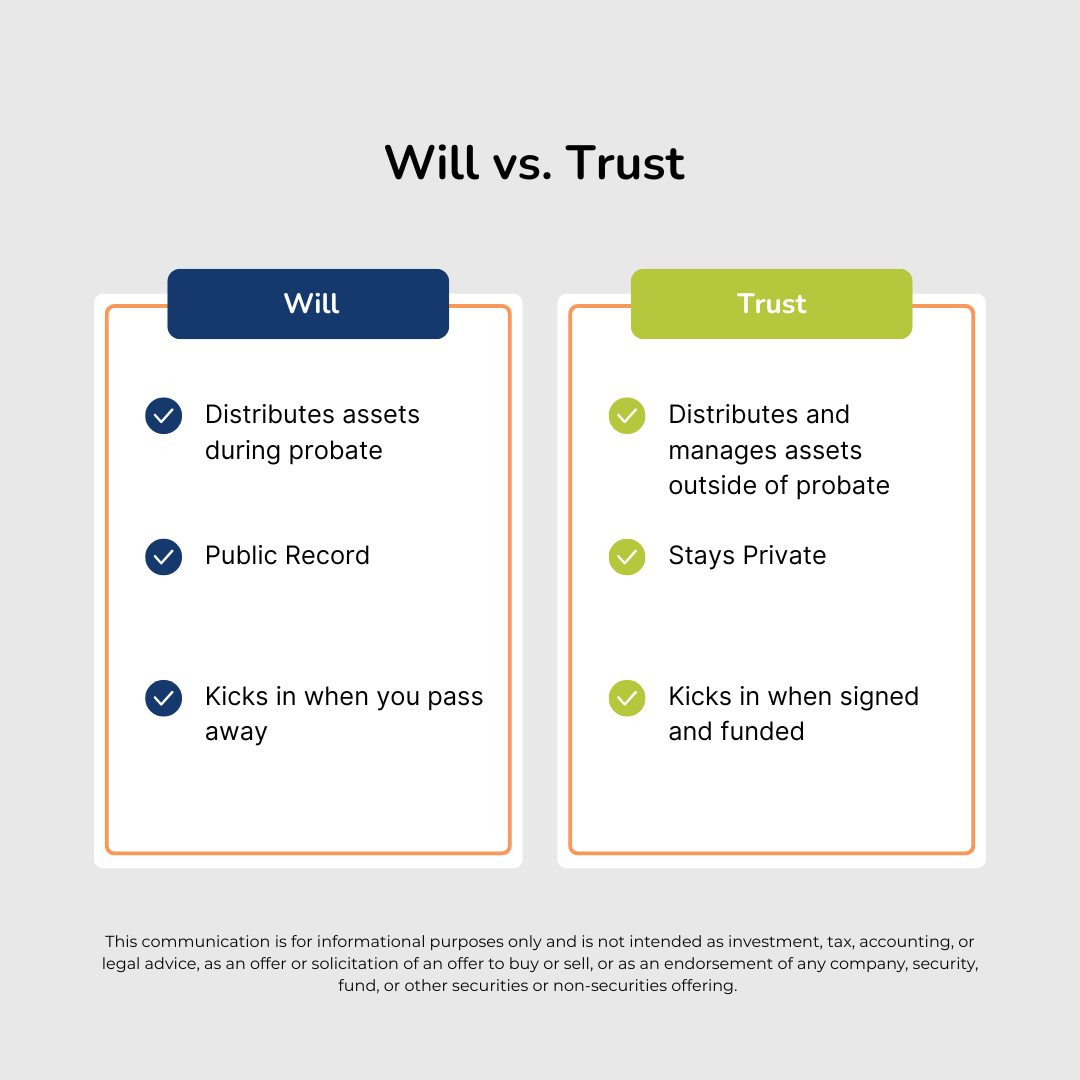

What is a Will?

Think of a will as the instruction manual for your estate plan during the probate process. It’s the main legal document you’ll draft to spell out who gets your belongings and who should take care of your estate.

Your will focuses on these three things:

- Who gets your stuff: In your will, you state who you want to receive your financial and personal belongings that don’t already have a beneficiary.

- Who settles your estate: You’ll appoint an executor. This is the person responsible for paying your final bills, utilities, taxes, and ensuring your wishes are carried out.

- Who takes care of your minor children: A will also lets you designate a guardian if you have a young child.

Once you pass away, your will is submitted to the court-driven probate process in the county where you live. It also becomes public, meaning anyone from your neighbor to a creditor can go to the probate court in your county and request to see what you owned and who you left it to.

What a Will Does Well

Here are the things that your will handles effectively:

- Simplicity: A will is a pretty straightforward and inexpensive estate planning document to create.

- Guardianship: If you still have minor children, your will is the only place you can legally nominate a guardian to take care of them.

- Instructions for Physical Property: A will lets you say who gets family heirlooms, furniture, jewelry, your house, or your cars. It’s pretty helpful because these items don’t have their own beneficiary form.

- Charitable Giving: Your will makes it easy to leave a portion of your estate to a charity or non-profit you care about.

- Protects Your Wishes: Probate gets a lot of flack, but by naming an executor and having the probate court oversee the process, your will provides a layer of protection. It makes sure that your bills are paid correctly and that your assets are distributed exactly how you want.

Limitations of a Will

You should have an updated will in place but know that it has its limits. It’s meant to specify who gets your things and how much they get. But if you want to control when or how your money is managed after you’re gone, a will by itself won’t help with that.

For example, maybe you want to specify that your grandchild gets portions of your estate over time so they don’t spend the money all at once. Or maybe you’re worried about an adult child that’s going through a divorce and how your money might go to the ex instead of your child. These situations can’t be protected by your will alone.

Another drawback is that your will has to go through the lengthy and costly probate process. In Ohio it usually takes six months to a year, or longer if things get messy. For a $1 million estate, the combined statutory executor and attorney fees could total $30,000 to $50,000 before your family ever sees a dime. And as I mentioned before, your will becomes public record. This means anyone can see the details of your estate, which often doesn’t sit well with the private nature of the people I serve.

It’s also not the most tax-efficient way of transferring your pre-tax retirement accounts like 401(k)s and IRAs. If your will distributes these accounts, your loved ones lose the 10-year window most heirs get to spread out the tax bill. Instead, the IRS often forces a 5-year or less payout. Because estate tax brackets are so compressed, they hit the top 37% tax rate in 2026 after just $16,250 in income. This means that leaving your IRA to your estate is essentially an invitation for the IRS to take a much bigger chunk.

What is a Trust?

Your will doesn’t kick in until you pass away, but a trust can be active the moment you sign and fund it. Unlike your will, a trust gives you control over how your money is managed and distributed, both while you’re alive and after you’re gone.

There are countless types of trusts, but for the sake of this discussion, I’ll be referring to the legal arrangement known as a revocable living trust. It’s a common estate instrument for the clients I work with. A revocable trust typically covers two main phases of life:

- While you’re living: You usually serve as your own trustee, meaning you keep full control over significant assets. If you become incapacitated, your trust can stay in control. It allows your successor trustee to step in and handle your bills or investments without the probate court needing to appoint a guardian.

- After you pass away: Unlike a will, which typically just says who gets your money, a trust lets you dictate the “how” and “when”. Also, your trust is a private document that bypasses probate, unlike your will which becomes public record.

Example: Let’s say you want to leave money to your grandchild. With a will, they might receive a large lump sum at age 18, before they’re ready to handle it. With a trust, you can specify that they receive portions over time or at specific ages.

For example, you could leave them one amount for college at age 19, another for a home down payment at 25, and the remainder at 30. You can even write in provisions that protect them from creditors or even a future divorce.

What a Trust Does Well

Here are the things your trust handles effectively:

- Avoids Probate: This is the most popular benefit of a trust. Assets held in your revocable trust bypass the probate court entirely. Your loved ones can access their inheritance in weeks rather than the six months to a year.

- Stays Private: Unlike your will, a trust doesn’t become a public record when you pass away.

- Planning for Incapacity: If you get to the point where you can’t manage assets yourself, your successor trustee can step in to pay your bills and handle your investments.

- Gives You Control: A trust lets you decide the how and when, where your will just states who gets your money. You can specify that a child or grandchild receives their inheritance over time or only after reaching certain life events, like graduating college.

- Asset Protection: You can protect the money you leave your loved ones from lawsuits, creditors, or even a future divorce.

Limitations of a Trust

The benefits of a trust come with some added complexity. One of the biggest hurdles is the upfront cost and effort. According to LegalZoom, in 2026, you can expect an attorney drafted revocable trust to cost between $1,500 to $4,000. For comparison, a will usually costs just a few hundred dollars.

Many of my clients are surprised to learn that you can’t just sign the trust documents and be done. You actually have to fund the trust by retitling your bank accounts, investments, and real estate into the trust’s name. Or you have to name the trust as your beneficiary.

If you forget that step, your assets will probably end up in probate court anyway, which defeats the point of having the trust. Even with a pour-over provision in your will sending assets to your trust, that still triggers probate.

You also have to be careful how you handle trust taxes. While you’re alive, a revocable trust doesn’t change your tax bill because the IRS just sees it as you. But after you pass away, any income that stays inside the trust is taxed at pretty steep rates.

According to SmartAsset, a trust hits the top 37% tax rate in 2026 after just $16,000 of income. For comparison, a married couple doesn’t hit that same 37% bracket until their income is over $768,700. If your trustee isn’t careful, the IRS could end up taking a much larger chunk of your money.

Key Differences Between a Will and a Trust

| Feature | Will | Trust |

| When it kicks in | Only after death | Once signed and funded |

| Probate required | Yes, court driven | No, bypasses the court |

| Privacy | Public | Private |

| Upfront cost | Usually a few hundred dollars | $1,500-$4,000 for attorney drafting |

| Tax efficiency | Risk of 37% tax rate on IRAs left to estate | Can be managed to minimize taxes |

| Control | Ends at distribution | Controls the how and when |

Do I Need a Will, a Trust, or Both?

The question “Do I need a will or a trust?” is a bit misleading. In most cases, this is really a choice between having only a will or having a will and a trust.

If you decide a trust is right for you, you’ll still want to have a will with pour-over provisions written in. These help make sure that if you forget to move an asset into your trust (like a new bank account or a car), that it eventually ends up in your trust.

Without a will, any assets left in your individual name (without a beneficiary) would be subject to your state’s intestacy laws. These are state rules that decide who gets your property based on your family tree, regardless of what you wanted.

In Ohio, dying without a will can complicate things if you have children from a previous marriage. Your current spouse might only be entitled to a portion of your estate. According to the Ohio Revised Code, your spouse might receive the first $20,000 plus a fraction of the remaining balance, with the rest going to your children. This could leave them without enough money to generate the retirement income they’ve been living on.

It’s also worth noting that some parts of your financial life might not need a will or a trust to find their way to your loved ones. Assets like life insurance policies, 401(k)s with listed beneficiaries, or bank accounts set up as ‘Payable on Death’ (POD) bypass probate entirely.

When a Will May Be Enough

If your financial picture is pretty simple, a will (in combination with Power of Attorney, Healthcare Power of Attorney, and Living Will) might be enough. This is especially true if you:

- Own just one home and have modest savings: If your estate is under a certain amount and your assets are straightforward, the costs of a trust might not outweigh the benefits.

- Don’t have minor children: You don’t need the managed inheritance features that trusts are helpful with.

- Aren’t concerned about privacy: You’re okay with the fact that your will becomes public record once it enters probate.

- Don’t have goals to spread out your money: You’re comfortable with your loved ones receiving their inheritance in a lump sum rather than payouts over time.

- Want to keep things simple: You’d rather avoid the upfront cost and effort of funding a trust and are confident that your insurance and investment beneficiary designations are up to date.

When a Trust and a Will May Make More Sense

A revocable trust and a will is the common setup for my clients with significant assets (at least $750,000 to $1,000,000+). You might lean toward a trust and will if you:

- Want to avoid probate: You want to save your family time, stress, and the costs that come with a lengthy court process.

- Value privacy: You don’t want your estate and wishes to become public record for your nosy neighbors.

- Own property in multiple states: If you have a cabin in North Carolina or a beachfront condo in Florida, a trust helps you avoid ancillary probate (additional probate in each state where you own property).

- Have a blended family: Trusts are great tools for distributing money in complicated family structures, helping you avoid accidental disinheritance.

- Build protection into your plan: Maybe you have minor children or an adult child who isn’t ready to handle a large sum of money. A trust lets you protect your estate from creditors, lawsuits, or even divorce.

- Own a business: Business succession planning can go much smoother with a trust in place to keep the lights on while transition is taking place.

Common Estate Planning Example Scenarios

You’re Caring for Grandchildren

Maybe you’ve stepped in to help raise your grandkids and named a relative as their guardian in your will. Your will says who will care for them, but you also have a trust that makes sure that their college funds or inheritance doesn’t just sit in a court-monitored account until they turn 18. Your successor trustee can use that money immediately for their private school, sports, or healthcare, releasing the rest in stages or when they’re mature enough to handle it.

Retired with Significant Assets

You’ve spent decades building your estate to around $1.8 million dollars. By using a trust and a will, you’ve made sure that if you pass away, your spouse and eventually your children or grandchildren can access your accounts and investments without waiting months for a probate court to grant permission.

Blended Families and Gray Divorce

You’ve remarried later in life and have children from your first marriage. You want to make sure your current spouse can stay in your home, but you’re worried your biological children might eventually be cut out. The right trust can give your spouse income and housing for their lifetime, while creating a legal guarantee that your remaining money will go directly to your kids once your spouse passes away.

You Have Property in Multiple States

You own your primary home here in Ohio and a beachfront condo in Florida or a cabin in the Carolinas. Without a trust, your children would be forced to hire different attorneys and open separate probate cases in each state. Because your out-of-state property is titled in your trust, your family bypasses ancillary probate entirely.

Common Mistakes to Avoid

You’ve worked hard to get a will or a will and a trust in place. Here are the most common estate planning mistakes I caution my clients about:

- Failing to fund your trust: Unfortunately I see this all of the time. You can have a beautifully drafted trust, but if you don’t retitle your bank or trust company accounts, investments, and real estate into the trust’s name (or make the trust your beneficiary), it’s basically useless. Any assets left in your own name will still have to go through probate court.

- Outdated beneficiaries: Most people don’t realize that the beneficiaries listed on your IRA, 401(k), and life insurance policies override your will or trust. If you haven’t updated them since a divorce or the birth of a grandchild, your money could legally go to the wrong person.

- The risk of joint ownership: Some retirees try to avoid probate by adding an adult child as a joint owner on their bank account or home. This can be risky. If your child gets sued, files for divorce, or has a tax lien, your money or home could be seized to cover their debts.

- Not planning for incapacity: Estate planning isn’t just about what happens after you pass away. If you don’t have an updated Power of Attorney or Healthcare Power of Attorney, your family might have to go to court to get permission to pay your bills or make medical decisions if you become ill. And they may not honor what you want to happen because you didn’t put it in writing.

- Forgetting to update after life events: Life in your 60s and 70s can be just as chaotic as your 40s. If you remarry, your estate plan from ten years ago might accidentally disinherit your biological children or leave your current spouse in a bind.

- Ignoring digital assets: In 2026, so much of our lives are online. If you haven’t left instructions or access to your digital photos, social media accounts, or cryptocurrency, those assets could become a nightmare for your family.

Final Thoughts

Still on the fence about whether you need a trust or just a will? Give some thought to how important it is for your estate to stay a private rather than a public court record. Ask yourself whether your family would benefit from accessing your accounts in a few weeks rather than waiting out a six-to-twelve-month probate process. Also consider if you want to control how and when your loved ones receive your money, especially if you’re worried about a large lump sum being managed poorly. If privacy, speed, and control are high priorities for you, then moving forward with both a trust and a will might be a good decision.

To help you find an attorney to draft your estate documents, you could search the American College of Trust and Estate Counsel (ACTEC) directory and the Ohio State Bar Association for lawyers who are specifically certified in Trust and Probate law. If you have a tight budget or simple financial situation, online vendors like Trust & Will or LegalZoom are popular options for digital estate document creation. Also be sure to consult your financial advisor to make sure your estate documents fit into your financial plan.

Want Help Navigating Your Financial Situation? Contact Stage Ready Financial Planning for a No-Commitment Consultation

Deciding whether you need a will or a trust is just one part of orchestrating a successful retirement. Stage Ready Financial Planning helps you look at the big picture, from the tax benefits of your estate plan to how you’ve set up your investments, so you can focus on the music of a life well lived.

While I don’t provide legal or tax advice, I work alongside your estate planning attorney to make sure your strategy is seamless. If you’ve saved $750,000 or more and want to make sure your plan is set up correctly, let’s talk. Schedule your intro call today!

Frequently Asked Questions (FAQs)

Do I need a trust or is a will enough?

A will might be enough If your financial picture is simple. This would be true if you own one home, have modest savings, and no minor children. But if you have a large or complex estate, own property in other states, or have a blended family, a will alone won’t provide the privacy or control you need. Adding a trust would help you plan for these challenges and control how your estate is handled when you’re gone.

Can you have both a will and a trust?

Absolutely and in most cases, you should. Most of the attorneys I’ve worked with use a pour-over will alongside a revocable living trust. You can think of the pour-over provision as a safety net. If you forget to move something into your trust (like a new car or a bank account), that asset is moved into the trust after you pass away. Note that the pour-over will still goes through probate.

What are the disadvantages of having a trust?

The main disadvantages of setting up a trust include the upfront cost and the ongoing maintenance. You’re looking at higher fees ($1,500 – $4,000) to have an attorney draft a trust compared to a few hundred for a basic will. You also have the responsibility of funding the trust, which means retitling your houses, accounts, and investments into the trust’s name (or naming the trust as your beneficiary). If you don’t fund it, the trust is basically an empty instrument.

What happens if you die without an estate plan?

Without a will or trust, you die “intestate.” Your state’s rigid laws get to decide who inherits your belongings, regardless of what you want. For example, in Ohio, if you have children from a previous marriage, the state might split your money between them and your current spouse in a way that leaves your spouse without enough income to live on. Essentially, the state writes your will for you, and they rarely get the details right.

About the Author

Joseph A. Eck, CFP®, is the owner and lead financial advisor at Stage Ready Financial Planning. He’s dedicated to helping retirement savers like you achieve peace of mind by creating a solid estate plan. With a background in education, and over a decade in wealth management, Joseph provides a conductor’s ear for detail, ensuring your investments, taxes, and estate planning documents work in perfect harmony.

Article References

- Trust & Will. “2026 Estate Planning Report: Key Findings and Trends.” Accessed April 27, 2026. https://trustandwill.com/learn/estate-planning-report-2026

- Ohio State Bar Association. “Law Facts: Probate.” Accessed April 27, 2026. https://www.ohiobar.org/public-resources/commonly-asked-law-questions-results/law-facts/law-facts-probate/

- Mizak & Pacetti Attorneys at Law. “How Long Does Probate Take in Ohio?” Accessed April 27, 2026. https://mizakandpacetti.com/how-long-does-probate-take-in-ohio/

- U.S. Bank. “Will vs Living Trust vs Living Will for Estate Planning.” Accessed May 4, 2026. https://www.usbank.com/wealth-management/financial-perspectives/trust-and-estate-planning/will-vs-living-trust-vs-living-will.html

- LegalZoom. “How Much Does a Living Trust Cost? (2026 Price Guide).” Accessed May 4, 2026. https://www.legalzoom.com/articles/cost-to-set-up-a-living-trust

- SmartAsset. “Trust Tax Rates and Exemptions for 2026.” Accessed May 4, 2026. https://smartasset.com/taxes/trust-tax-rates

- Nolo. “Intestate Succession in Ohio: Who Inherits When There’s No Will?” Accessed May 4, 2026. https://www.nolo.com/legal-encyclopedia/intestate-succession-ohio.html

- Ohio Revised Code. “Section 2105.06: Statute of Descent and Distribution.” Accessed May 4, 2026. https://codes.ohio.gov/ohio-revised-code/section-2105.06

- American College of Trust and Estate Counsel (ACTEC). “Find an ACTEC Fellow: Peer-Elected Trust and Estate Attorneys.” Accessed May 4, 2026. https://www.actec.org/find-a-lawyer/

- Ohio State Bar Association. “Attorney Directory: Board Certified Specialists in Estate Planning, Trust and Probate Law.” Accessed May 4, 2026. https://www.ohiobar.org/public-resources/find-a-lawyer/

- Trust & Will. “Online Estate Planning: Create a Will or Trust in Minutes.” Accessed May 4, 2026. https://trustandwill.com/

- LegalZoom. “Estate Planning Services: Wills, Living Trusts, and Power of Attorney.” Accessed May 4, 2026. https://www.legalzoom.com/personal/estate-planning/

This communication is for informational purposes only and is not intended as investment, tax, accounting, or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision. Past performance is no indication of future results.