Updated: January 7th, 2026

Does understanding your taxes make your head spin? Are you planning to sell something and wonder if you will have a state of Ohio capital gains tax? You aren’t alone and the good news is that we’ve got you covered!

As an Ohio resident, understanding your capital gains tax is important when you are buying, selling, or investing in property and securities. This guide will walk you through the important points you need to know and share strategies to help you potentially reduce your capital gains tax liability.

Article Key Takeaways

- Ohio Doesn’t Have a Separate Capital Gains Tax: Ohio taxes your capital gains as regular income, meaning they’re subject to the state’s income tax brackets based on your adjusted gross income (AGI).

- Federal Capital Gains Tax Rates Vary: Federal capital gains taxes depend on whether your gains are short-term or long-term as well as your taxable income and filing status. Long-term capital gains can have more favorable rates if you are in a high tax bracket.

- Strategies Exist to Minimize Your Taxes: Several strategies can help reduce both federal and Ohio capital gains taxes. Consulting with a financial planner and tax professional can provide you with personalized guidance.

What Are Capital Gains?

Capital gains are the profits you earn from selling a “capital asset” for more than you paid for it. Examples of “capital assets” include stocks, bonds, real estate, vehicles, etc.

Even before you sell an asset, you can have a capital gain if the value of your item has increased since you purchased it. On the contrary, you might have a capital loss if the item you own has depreciated since you purchased it.

Gains or losses for assets that haven’t been sold yet are called “unrealized” capital gains or “unrealized” capital losses. You won’t have a capital gain tax liability until you actually sell the asset. These are called “realized” capital gains.

Realized capital gains may be taxable, while realized losses can reduce your tax bill.

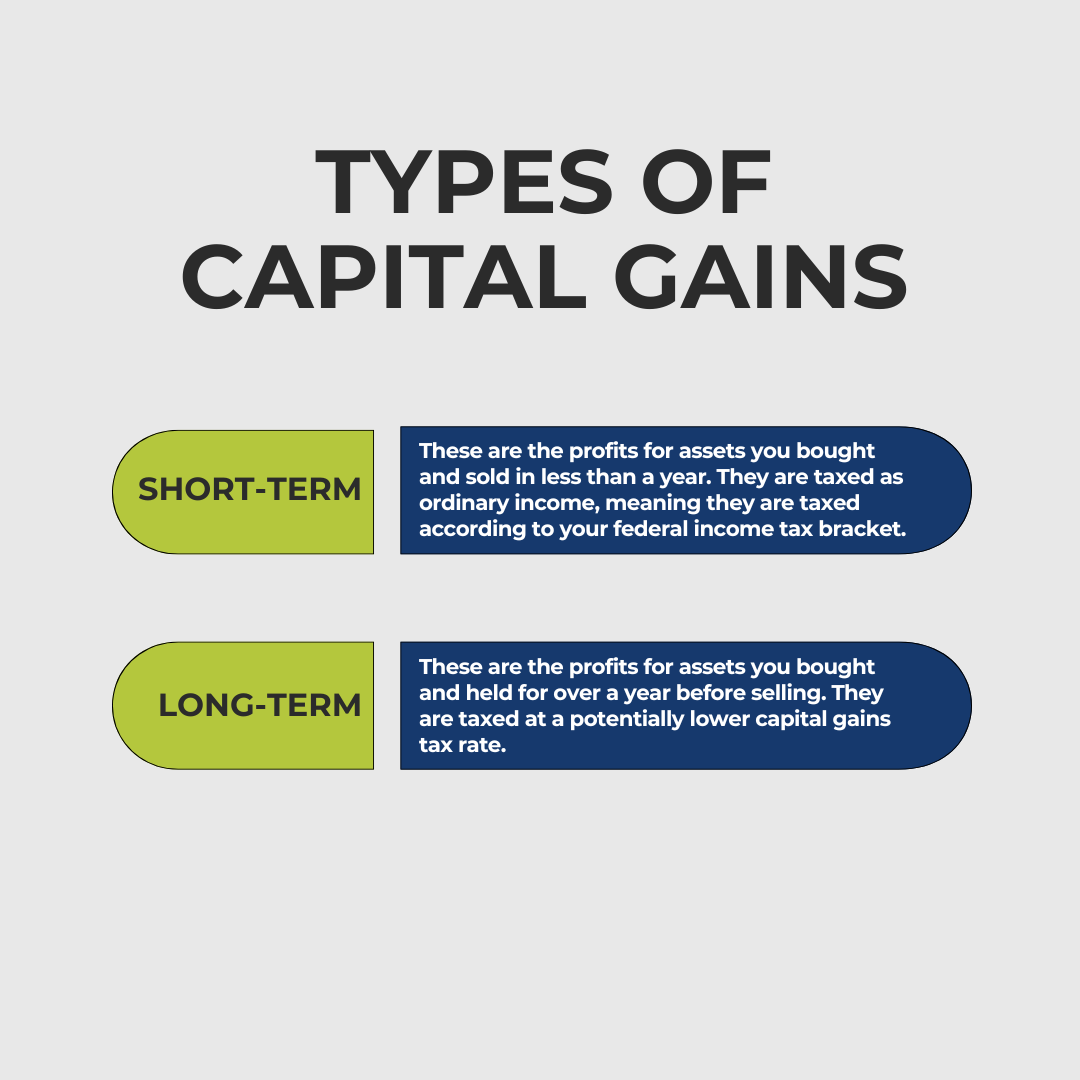

Types of Capital Gains

From a tax standpoint, your gains are categorized based on how long you owned the item you sold. There are two primary categories of capital gains:

- Short-Term Capital Gains: These are the profits for assets you bought and sold in less than a year. They are taxed as ordinary income, meaning they are taxed according to your federal income tax bracket.

- Long-Term Capital Gains: These are the profits for assets you bought and held for over a year before selling. They are taxed at a potentially lower capital gains tax rate.

How Your Capital Gains Are Taxed

First, it’s important to know if you have an “unrealized” or a “realized” capital gain. “Unrealized” capital gains are not taxed. Once you sell an asset, your gain becomes “realized” and you will potentially owe capital gains taxes.

Your capital gains tax rate is based on the following factors:

- The type asset you sell

- How long you owned the asset for before selling

- Your overall adjusted gross income and taxable income

What Is the Federal Capital Gains Tax?

The federal government specifically taxes your capital gains. The federal capital gains tax rates vary depending on a few different factors.

How Federal Capital Gains Tax Works

The federal government taxes capital gains income at different rates based on your taxable income and filing status:

Long-Term Capital Gains

Long-term capital gains tend to have more favorable tax rates compared to short-term capital gains. These gains are taxed depending on your federal taxable income at either 0%, 15%, or 20%.

| Filing Status in 2026 | LTCG 0% Rate | LTCG 15% Rate | LTCG 20% Rate |

| MFJ | $0 – $98,900 | $98,901 – $613,700 | $613,700+ |

| Single | $0 – $49,450 | $49,451 – $545,500 | $545,500+ |

*Tax Year 2026

Short-Term Capital Gains

These profits are taxed as ordinary income, based on your federal tax bracket.

| Tax Rate for 2026 | Filing MFJ | Filing Single |

| 10% | $0 – $24,800 | $0 – $12,400 |

| 12% | $24,801 – $100,800 | $12,401 – $50,400 |

| 22% | $100,801 – $211,400 | $50,401 – $105,700 |

| 24% | $211,401 – $403,550 | $105,701 – $201,775 |

| 32% | $403,551 – $512,450 | $201,776 – $256,225 |

| 35% | $512,451 – $768,700 | $256,226 – $640,600 |

| 37% | $768,700+ | $640,600+ |

*Tax Year 2026

Example of Federal Capital Gains Taxes

Let’s say you sell a stock in a brokerage account that you owned for two years for a $50,000 profit. This “realized” capital gain would be considered a long-term capital gain because you held the stock for over a year. Your federal capital gains tax rate would then depend on your income tax bracket.

For tax year 2026, if you file as single, and had federal taxable income (including your $50,000 gain) of $150,000, you would pay 15% federal capital gains tax on your profit.

Does Ohio Have a State Capital Gains Tax?

Ohio does not have a separate capital gains tax, instead it treats capital gains income as part of your overall taxable income. This means capital gains are subject to Ohio’s income tax brackets which are based on your “adjusted gross income.”

| Ohio Taxable Income (Adjusted Gross Income) | Rate According to Most Recent Update in 2025 |

| $0 – $26,050 | 0% of Ohio taxable nonbusiness income |

| $26,051 – $100,000 | $342.00 + 2.75% of excess over $26,050 |

| $100,001 + | $2,394.32 + 3.125% of excess over $100,000 |

*Tax Year 2025. Ohio’s income tax rate is set to adjust to a flat 2.75% for tax year 2026 and beyond for income over $26,050.

How Ohio Taxes Your Capital Gains

According to Section 5733.051 of the Ohio Revised Code, Ohio’s tax system determines if you have a capital gains tax liability based on where you sold your asset and where it was utilized.

Real Property

Capital gains tax liability from real property is determined based on the property’s location. Real property typically includes real-estate.

If you sell a house or piece of land that’s located in Ohio, your capital gain will likely be taxed by the state. As we will discuss later, there are exclusions for this tax liability when selling your primary residence.

Tangible Personal Property

Gains from tangible personal property are taxed based on their usage within Ohio. Tangible personal property includes items like your jewelry, clothing, vehicles, etc. If you sell one of these items for a gain and you used the item while living in Ohio, this gain is likely taxable in Ohio.

Intangible Property

These are gains from intangible assets such as stocks or securities. They are taxed based on residency. If you are an Ohio resident, you will pay state income tax on any gains you create for selling these assets.

Example of How Ohio Taxes Your Capital Gains

Let’s say you sell an investment property in Ohio for a $100,000 profit and you’ve owned the home for 10 years. By owning the home for over a year, this would count as a federal long-term capital gain. Since your property is located in Ohio, the gain would also be subject to Ohio’s state income tax.

In this example let’s say you filed as MFJ and your federal adjusted gross income was $200,000 (including your capital gain). After taking the standard deduction of $30,000, your federal taxable income was approximately $170,000. Your federal capital gains tax rate on the sale would be 15% and you would be in the 3.125% Ohio income tax bracket.

Strategies to Reduce Your Ohio & Federal Capital Gains Taxes

While taxes on capital gains can feel unavoidable, there are several smart planning opportunities that can help lower what you owe. By understanding how different rules apply to your income, investments, and property, you can take intentional steps to reduce your federal and Ohio tax burden.

Below are some of the most effective strategies to consider when planning ahead for your next major sale or investment decision:

- Leverage Your Primary Residence Exclusion

- Explore Tax-Loss Harvesting

- Keep Track of Your Cost Basis

- Hold Assets for Over a Year

- Maximize Your Pre-Tax Retirement Contributions

- Use Tax Efficient Investments

- Use a 1031 Exchange for Your Real Estate

- Take Advantage of the Inheritance Cost Basis Step-Up

- Consider Charitable Giving & Tax Exempt Trusts

1. Leverage Your Primary Residence Exclusion

If you are selling your home, you may be able to exclude up to $250,000 ($500,000 for married couples) in capital gains if you meet the ownership and use tests. According to the IRS, you need to have both owned the home and lived in it as your primary residence for 2 of the last 5 years.

2. Explore Tax-Loss Harvesting

You can offset your taxable income by pairing realized capital losses with your capital gains. If you know you will have a large capital gain, you might consider selling another investment or asset at a loss to offset your gain. You will pay tax on the net of your combined gains and losses. Be sure to learn more about tax rules that prohibit deductible losses, such as the wash-sale rule.

3. Keep Track of Your Cost Basis

The term ‘cost basis’ refers to the original price you paid for an asset. It’s wise to keep detailed records of your initial purchase price, as well as any upgrades, repair expenses, taxes paid, insurance costs, and loan interest.

These additional costs can typically be added to your original purchase price to calculate your true cost basis. A higher cost basis results in a lower capital gain.

4. Hold Assets for Over a Year

If you hold an asset for more than a year, you may be able to take advantage of potentially lower long-term capital gains tax rates. Since short-term capital gains are taxed as ordinary income, long-term gains can be more appealing if you are in a higher federal income tax bracket.

5. Maximize Your Pre-Tax Retirement Contributions

Contributions to your pre-tax 401(k), Traditional IRA, or Health Savings Account can reduce your adjusted gross income (AGI) and your taxable income. The lower your taxable income, the less you will pay in capital gains tax.

6. Use Tax Efficient Investments

Actively managed mutual funds often create higher capital gains tax liabilities than passive investments like index funds and ETFs. Actively managed investments have a fund manager who is trading on a regular basis, creating ongoing tax liabilities.

Passive investments like ETFs track an index and trade infrequently. This makes them a more tax efficient approach to investing.

7. Use a 1031 Exchange for Your Real Estate

A 1031 exchange allows you to defer your capital gains tax when selling an investment property by reinvesting the proceeds into a like-kind property. If you follow the IRS guidelines, you may be able to swap one property for another without immediately recognizing your gain, helping you delay or reduce your tax burden.

1031 exchanges are complicated and have strict rules. Be sure to work closely with your tax professional if you are interested in this tactic.

8. Take Advantage of the Inheritance Cost Basis Step-Up

When someone inherits your assets like real estate or stocks, their cost basis is “stepped up” to the asset’s fair market value on the day that you pass away. This means that if your heir sells your asset, capital gains are only calculated on any appreciation after they inherit it.

The cost basis step-up can potentially reduce or eliminate your original capital gains tax liability. Therefore, consider avoiding selling highly appreciated securities and instead leaving them to your heirs.

The cost basis “step-up” does not apply to investments that you own inside tax-deferred accounts like 401(k)s, traditional IRAs, and annuity contracts.

9. Consider Charitable Giving & Tax Exempt Trusts

If you donate your appreciated assets, such as stocks or real estate, you may be able to avoid paying capital gains tax on their appreciation while potentially qualifying for a charitable tax deduction.

If you have large “unrealized” capital gains, you might also consult with an attorney about using a tax-exempt trust such as a Charitable Remainder Trust (CRT).

When you transfer appreciated assets into a CRT, the trust itself is tax-exempt. This means the trust can sell those assets without incurring capital gains tax. The trust then provides income to you or your designated beneficiaries for a set period or for life. At the end of that period, the remaining trust assets are transferred to a charitable organization. However, it’s important to note that the income beneficiaries of the CRT will pay taxes on the income they receive.

How a Financial Planner Can Help You with Capital Gains Tax and More

Navigating Ohio’s state income tax on capital gains and federal capital gains taxes can be complex. A qualified financial planner can help you structure your investments to minimize your capital gains tax liability. They can provide you with strategy recommendations about reducing your income tax and improving overall tax efficiency.

Collaborating with your financial planner and your tax professional ensures that you are compliant with both state and federal government tax regulations.

Learn More about Stage Ready Financial Planning’s Personalized Approach to Tax Planning

Are you a retirement saver over age 50? At Stage Ready Financial Planning, we help you build a plan that aligns your resources with your goals in the most tax efficient way possible.

We strive to help you retire successfully, invest with confidence, and reduce your tax liability. Schedule your intro call today!

Frequently Asked Question (FAQs)

Do you pay Ohio income tax on capital gains?

Yes, Ohio taxes your capital gains as part of your individual state income tax. Some states have a separate state capital gains tax rate, however Ohio does not. Your tax bracket is determined by your adjusted gross income in Ohio. For tax year 2025, Ohio’s state income tax ranges from 0% to 3.125% and is set to drop to a flat 2.75% for tax year 2026 and beyond for income exceeding $26,050.

How do I avoid capital gains tax in Ohio?

Because Ohio taxes your capital gains just like any other income you earn, the lower your adjusted gross income, the less you will pay in taxes. Some common strategies to accomplish this include: tax-loss harvesting, holding assets for more than a year, and utilizing your primary residence exclusions. See the list above for a more comprehensive set of ideas.

About the Author

Joseph A. Eck, CFP®, is a financial planner passionate about helping retirement savers achieve their financial goals and reduce their lifetime tax liability. With years of experience in tax planning, retirement planning, and investment management, Joseph provides personalized guidance and support to clients in Dayton and Southwest Ohio. He believes that everyone deserves to feel confident living their ideal retirement and keeping more of their hard earned savings. Click here to learn more about Joseph.

Article References

- https://codes.ohio.gov/ohio-revised-code/section-5733.051

- https://www.irs.gov/taxtopics/tc701#:~:text=Qualifying%20for%20the%20exclusion&text=You’re%20eligible%20for%20the,during%20different%202%2Dyear%20periods.

- https://www.investor.gov/introduction-investing/investing-basics/glossary/wash-sales#:~:text=A%20wash%20sale%20occurs%20when,to%20buy%20substantially%20identical%20securities.

- https://www.investopedia.com/financial-edge/0110/10-things-to-know-about-1031-exchanges.aspx

- https://www.irs.gov/pub/irs-news/fs-08-18.pdf

- https://www.investopedia.com/terms/s/stepupinbasis.asp

- https://www.irs.gov/charities-non-profits/charitable-remainder-trusts

This communication is for informational purposes only and is not intended as investment, tax, accounting, or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision. Past performance is no indication of future results.