Updated: March 24th, 2026

If you’re over 50 and thinking about withdrawing from your retirement accounts, you’ll need to understand how to calculate your 401(k) withdrawal tax rate. Without a plan, you could end up paying more to the IRS than you need to. But with the right strategy, you can keep more of your hard earned savings and enjoy your retirement income.

This article breaks down how 401(k) withdrawals are taxed and how your investment distributions impact your federal and state tax rates and strategies to help you avoid an IRS surprise.

Article Key Takeaways

- Understand How Taxes Impact Your 401(k) Withdrawals: Learn how federal and state taxes apply to your distributions and why your income level matters.

- Know the Rules to Avoid Penalties: Avoid early withdrawal penalties and learn about exceptions for medical expenses, emergencies, and rollovers.

- Strategize for a Tax-Efficient Retirement: Plan withdrawals wisely to stay in lower tax brackets and optimize your income.

Understanding How 401(k) Withdrawals Are Taxed

Withdrawals from your pre-tax 401(k) are subject to federal and sometimes state income taxes. This is because pre-tax 401(k) contributions receive an up-front tax deduction, meaning they haven’t been taxed yet.

If you made Roth or after-tax contributions to your 401(k), you may be able to make tax-free withdrawals. This works because Roth or after-tax 401(k) contributions don’t qualify for a deduction when the money goes into the account, meaning you’re paying tax on your contributions.

What Is the Tax Rate on 401(k) Withdrawals?

Your 401(k) withdrawal federal tax rate depends on your total income, including from your investments, Social Security, and pensions. The higher your overall taxable income, the higher your income tax rate.

According to the IRS, here are the 2026 federal tax brackets for those who file their return as Married Filing Jointly:

| MFJ Taxable Income | Tax Rate |

| $0 – $24,800 | 10% |

| $24,801 – $100,800 | 12% |

| $100,801 – $211,400 | 22% |

| $211,401 – $403,550 | 24% |

| $403,551 – $512,450 | 32% |

| $512,451 – $768,700 | 35% |

| $768,700+ | 37% |

*Tax Year 2026

Example: For tax year 2026 A married couple, both age 62, have an adjusted gross income (AGI) of $100,000. Filing jointly, they take the $32,200 standard deduction, leaving them with $67,800 in taxable income, placing them in the 12% tax bracket.

If they withdraw $36,200 from their 401(k)s, their taxable income rises to $104,000, pushing a portion of their income into the 22% tax bracket.

Important Note: Only the portion above $100,800 (the 12% bracket limit for 2026) is taxed at 22%. Their first $100,800 remains taxed at lower rates.

When Do You Pay Taxes on 401(k) Withdrawals?

You will owe federal and potentially state income taxes on your pre-tax 401(k) withdrawals for the calendar year that you take money out. Your 401(k) custodian will report your distributions to the Internal Revenue Service (IRS). You’ll receive a 1099-R the following spring that shows how much you took out along with any taxes that were withheld.

Most 401(k) plan distributions require at least 20% federal tax withholding, and some states also have minimum withholding rules. If you want to withhold less than 20% federal, you may need to roll your 401(k) into a Traditional IRA for more flexibility.

Assuming you’ve withheld enough federal and state income taxes from your 401(k) distributions to fully cover your tax liability, then you won’t owe anything more come the following April. If you under withhold, you might owe additional taxes or underpayment penalties.

What Are Required Minimum Distributions (RMDs)?

Required minimum distributions (RMDs) are withdrawals that you have to take from your pre-tax retirement accounts as you get older. They’re designed by the IRS to make sure that your retirement savings are eventually used and taxed rather than left to grow tax-deferred indefinitely.

The SECURE 2.0 Act changed the age that your RMDs need to start. According to the IRS, once you reach age 73, you must begin taking required minimum distributions (RMDs) from your pre-tax 401(k) or any pre-tax retirement account. These used to start at age 70.5.

- Your first RMD must be taken by April 1st of the year following the year you turn 73.

- All subsequent RMDs are due by December 31st each year.

- In 2033, the RMD age is set to increase to 75 under current laws.

How Are My RMDs Calculated?

Each year, your RMD is determined by dividing your prior year-end (December 31st) retirement account balance by a life expectancy factor found in the IRS Uniform Lifetime Table. The larger your balance and the lower your life expectancy factor, the higher your required withdrawal.

You can use the IRS RMD Worksheet or an online RMD calculator to estimate your required distribution.

Are There Penalties for Missing RMDs?

RMDs are taxed at your ordinary income tax rate, just like any other 401(k) withdrawal. If you fail to take your full RMD, the IRS currently imposes a penalty of 25% of the amount not withdrawn. This penalty is on top of the income tax due for your missed RMD.

Are There Any Exceptions to RMDs?

- Still Working: If you’re still employed and participating in your employer’s 401(k), you might be able to delay RMDs from that plan but not from your other retirement accounts.

- Roth 401(k) RMD Rule Change: Roth 401(k)s are no longer subject to RMDs, aligning them with the rules for Roth IRAs.

RMDs force you to claim additional taxable income, which could push you into a higher tax bracket. Later in the article, we’ll discuss strategies to manage RMDs, including strategic withdrawals, Roth conversions, and Qualified Charitable Distributions (QCDs).

What Is the Early Withdrawal Penalty for a 401(k)?

If you withdraw funds from your 401(k) before age 59.5, you might face a 10% early withdrawal penalty in addition to the income taxes you owe for the distribution. The IRS penalty discourages early withdrawals, which can significantly reduce your retirement savings over time.

According to the IRS, there are exceptions where you can avoid the penalty, including:

- Rollovers: Transfers from one retirement plan directly to another retirement plan within 60 days typically avoids taxes and the 10% penalty.

- Disability: If you become permanently disabled, you may take early withdrawals without the penalty.

- Personal Emergency Expense: 401(k) plans now allow one penalty-free withdrawal per year for personal emergency expenses. The amount is up to the lesser of $1,000 or the vested account balance over $1,000.

- Medical Expenses: Withdrawals used to cover medical expenses that exceed 7.5% of your adjusted gross income (AGI) may avoid the penalty.

- Early Separation from Employment: If you leave your job between age 55 and 59.5, you may be able to take 401(k) withdrawals without a penalty. Federal and state taxes will still apply. This exception does not apply to IRAs.

- Qualified Domestic Relations Order (QDRO): If the withdrawal is made due to a divorce settlement, the penalty may be waived.

- Birth or Adoption of a Child: You may withdraw up to $5,000 penalty-free for birth or adoption expenses.

Important Note: Even if an exception applies, you may still owe federal and state income taxes on your withdrawal. Always check with your tax professional before taking distributions.

How Do State Taxes Affect Your 401(k) Withdrawal?

Your 401(k) withdrawal may also incur state taxes depending on where you live. Some states have an income tax and some don’t. Additionally, there are states with an income tax that don’t tax retirement income.

The following chart outlines how different states tax 401(k) withdrawals::

| States With No Income Tax | Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington, Wyoming, New Hampshire |

| States With An Income Tax That Don’t Tax Retirement Income | Illinois, Iowa, Mississippi, Pennsylvania |

| States With An Income Tax That Tax Retirement Income | All Others |

Example: Lets say you are already in the 22% federal tax bracket and your state has an income tax of 3.125% on retirement income. If you withdraw an additional $10,000 from your 401(k) and it doesn’t push you into another tax bracket, you would owe:

- Federal tax: $2,200 (22% of $10,000)

- State tax: $312.50 (3.125% of $10,000)

- Total taxes due for this withdrawal: $2,512.50 (or 25.125%)

How Do Ohio State Taxes Affect Your 401(k) Withdrawal?

In Ohio, the state tax rate on all income, including 401(k) withdrawals follows a progressive system. Ohio determines your tax bracket based on your adjusted gross income.

Here’s a quick breakdown of the current Ohio state tax brackets as of 2025:

| Adjusted Gross Income | Tax Year 2025 – Ohio State Tax Rate |

| $0 – $26,050 | 0% |

| $26,051 – $100,000 | $342.00 + 2.75% of excess over $26,050 |

| $100,000 + | $2,394.32 + 3.125% of excess over $100,000 |

*Tax Year 2025. Ohio’s income tax rate is set to adjust to a flat 2.75% for tax year 2026 and beyond for income over $26,050.

Example: A married couple who are both age 62 have an adjusted gross income of $90,000 placing them in the 2.75% Ohio tax bracket. If they file jointly and take the $32,200 federal standard deduction, they would have taxable income of approximately $57,800. This places them in the 12% federal tax bracket.

Withdrawing $46,200 more would raise their taxable income to $104,000 and adjusted gross income to $136,200. This would move them into the 22% federal tax bracket and the 3.125% Ohio tax bracket. This means a portion of their new income will be taxed at higher rates, increasing their overall tax bill. (This example uses 2026 federal rates an 2025 Ohio rates due to the date of publishing)

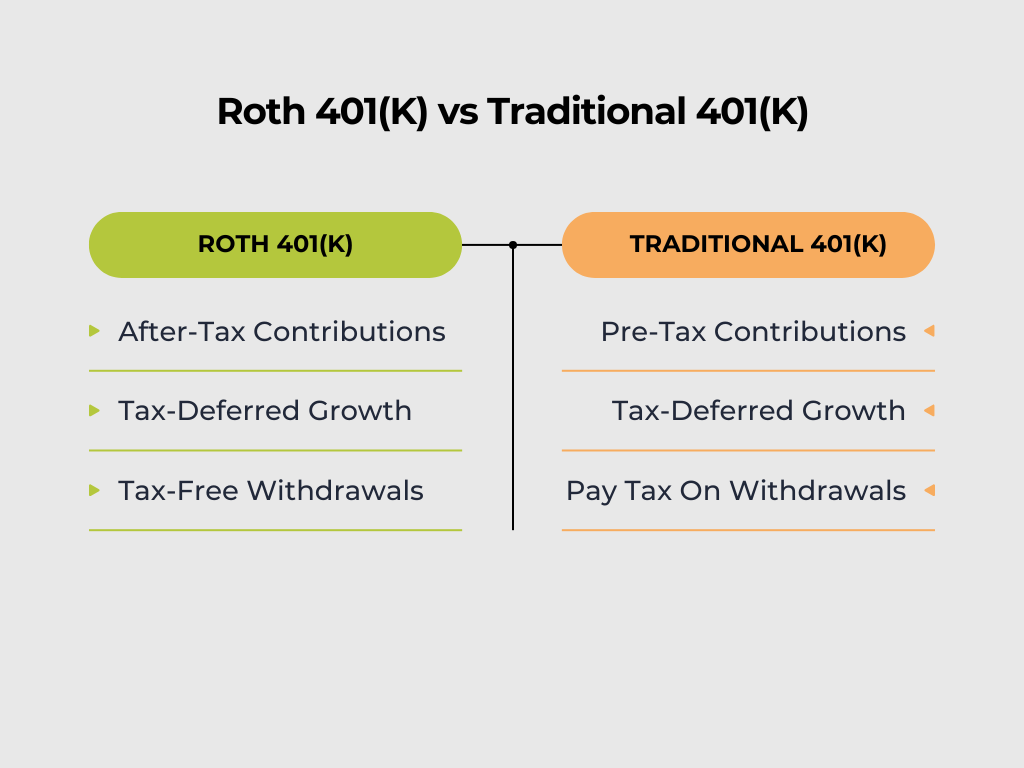

Roth 401(k) vs. Traditional 401(k)

A Roth 401(k) and Traditional 401(k) differ significantly in their tax treatment. The following tax rules also apply to Traditional IRAs and Roth IRAs respectively.

- Roth 401(k): Contributions are made with after-tax dollars. This means you won’t pay income taxes on your distributions provided you meet the requirements.

- Traditional 401(k): Contributions are made with pre-tax income. You will pay federal and possibly state income taxes when you take money out in retirement.

How to Minimize Taxes on 401(k) Withdrawals

There are several strategies to help reduce the tax burden of your 401(k) withdrawals. Be sure to consult with your financial planner and tax professional before trying any of the following:

- Roth Conversions: You can convert your pre-tax 401(k) or Traditional IRA funds into Roth dollars. Roth 401(k) and Roth IRA withdrawals are generally tax-free if the account is over five years old and you’re over 59.5. You’ll pay taxes on the amount you convert in the year you complete the conversion.

- Strategic Withdrawals: You could take account distributions in a way that minimizes your taxable income, helping you avoid higher tax brackets. Some common withdrawal strategies include:

- Withdrawing just enough to avoid moving into the next tax bracket or IRMAA Medicare premium tax bracket

- Distributing more income early in retirement to reduce RMD tax impacts at age 73 and later

- Qualified Charitable Distributions (QCDs): In 2026, the IRS allows you to transfer up to $111,000 ($222,000 per couple) of your RMD directly from your 401(k) or IRA to a charity. This allows you to avoid paying taxes on a portion of your RMD and support your favorite causes at the same time.

How to Plan Your 401(k) Withdrawals for Retirement

Here are the basic steps to follow if you’re planning your 401(k) withdrawals in retirement:

- Calculate Your Income Need: The first step is to determine how much net retirement income you need to support your ideal life. Start with building a clear budget based on your real spending history and then include extra for increased healthcare, lifestyle, and travel costs.

- Include Fixed Income: Next, you’ll need to subtract the net fixed income you’ll receive from sources like Social Security and pensions. This will help you assess how much additional money is needed from your 401(k) or IRAs to hit your income goal.

- Work Backwards to Determine Your Tax Withholding: Work with your financial planner and tax professional to determine the amount of federal and state income tax you should withhold based on the remaining net income you’ll need to create from your investments.

Example

- After reviewing your spending history, you determine you’ll need $10,000/mo in net retirement income to support your ideal lifestyle.

- If your net Social Security income is going to be approximately $5,000/mo between you and your spouse, you’d subtract that from $10,000. Now you know you’ll need to create $5,000 more in net retirement income from your 401(k) or other investments.

- Let’s assume you’ll pull the remaining amount from your pre-tax 401(k) and your tax professional and financial planner have helped you determine that you’ll need to withhold a total of 20% between federal and state income taxes. This means that in order to create $5,000/mo in net income and withhold 20% for taxes, you’ll need to withdraw $6,250/mo from your 401(k).

Consult with a Retirement Professional

A professional can help you minimize retirement taxes while maximizing your income. Consider working with a financial planner AND a tax professional to help you create a well rounded income strategy.

Discover How Stage Ready Financial Planning Helps You Retire with Confidence

Stage Ready Financial Planning specializes in helping clients in Dayton & Southwest, Ohio make informed decisions about their 401(k) withdrawals in retirement. We’ll guide you through annual tax planning, navigating RMDs, and more to ensure you retire with a steady and tax efficient monthly paycheck. Schedule your intro call today!

Frequently Asked Questions (FAQs)

How much do you pay in taxes for a 401(k) withdrawal?

The amount you’ll owe in taxes depends on your federal and state tax bracket. Your 401(k) withdrawals will be subject to federal income tax and potentially state income tax depending on where you live. In many cases you’ll have to withhold at least 20% in federal taxes due to your 401(k) plan rules. To avoid this, you could consider rolling your 401(k) into a Traditional IRA for increased flexibility.

How do I avoid a 20% tax on 401(k) withdrawal?

A mandatory 20% withholding usually applies if you’re taking money directly out of your 401(k). You can avoid this by rolling your 401(k) to an IRA. That said, if you’re taking money out between age 55 and 59.5, you’ll need to take distributions from your 401(k) to avoid the 10% IRS penalty for early withdrawals. Be sure to consult with your tax professional.

How do I calculate 401(k) early withdrawal taxes?

When withdrawing prior to age 59.5 from a 401(k), income taxes will apply as well as potentially a 10% penalty unless you qualify for an exception. Work with a tax advisor and financial professional to calculate how much you’ll need to pay in taxes.

About the Author

Joseph A. Eck, CFP®, is the owner and lead financial planner of Stage Ready Financial Planning. He’s passionate about helping retirees and retirement savers over age 50 achieve their financial goals and reduce their lifetime tax liability. With years of experience in tax planning and retirement planning, Joseph provides personalized guidance and support to clients in Dayton and Southwest Ohio. He believes that everyone deserves to feel confident living their ideal retirement. Click here to learn more about Joseph.

Article References

- Internal Revenue Service. “IRS releases tax inflation adjustments for tax year 2026, including amendments from the One, Big, Beautiful Bill.” Accessed March 24, 2026. https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2026

- Internal Revenue Service. “Retirement plan and IRA required minimum distributions FAQs.” Accessed March 24, 2026. https://www.irs.gov/retirement-plans/retirement-plan-and-ira-required-minimum-distributions-faqs

- Internal Revenue Service. “Publication 590-B (2025), Distributions from Individual Retirement Arrangements (IRAs).” Accessed March 24, 2026. https://www.irs.gov/publications/p590b

- Internal Revenue Service. “Required Minimum Distribution Worksheets.” Accessed March 24, 2026. https://www.irs.gov/retirement-plans/plan-participant-employee/required-minimum-distribution-worksheets

- Internal Revenue Service. “Retirement topics — Exceptions to tax on early distributions.” Accessed March 24, 2026. https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-exceptions-to-tax-on-early-distributions

- Ohio Department of Taxation. “Annual Individual Income Tax Rates.” Accessed March 24, 2026. https://tax.ohio.gov/individual/resources/annual-tax-rates

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision. Past performance is no indication of future results.