You’ve settled into retirement, and you’re feeling good about your monthly income. You’re bringing in even more than you thought you would and have some extra cash building up in the bank. If that sounds familiar, you might be wondering about how to best give money to your children and grandchildren.

Many of the families I work with in Dayton and Southern Ohio aren’t trying to live a flashy lifestyle, and they aren’t trying to make their kids rich. They just want to know their kids are taken care of. At the same time, they’d also prefer not to pay more federal income tax or gift taxes than they need to.

In this article, we’ll break down the common ways to give money strategically to your loved ones so that you can reduce the noise of retirement taxes.

Key Takeaways

- In 2026, you can give up to $19,000 per person annually without filing a gift tax return. Married couples can double this to $38,000 per recipient.

- Ohio residents can deduct gifted contributions up to $4,000 (single) or $8,000 (joint) per 529 beneficiary from their Ohio taxable income, with unlimited carry-forward for larger gifts.

- Unlike the IRS rules, Ohio Medicaid has a 5-year gifting look-back period. Any gifts made during this time could delay your eligibility for Medicaid long-term care coverage.

Why Gifting During Retirement Matters

The families I serve usually aren’t focused on legacy planning. In fact they often share in one of our first meetings that they don’t plan to make their kids rich when they die. Instead, they just want to see their hard-earned money go to things like their adult child’s wedding or a new home rather than the IRS.

The good news is that giving money to your kids or grandkids during retirement can be a smart strategy. There are both tangible tax benefits and intangible perks to retirement gifting, including:

- Reducing future RMDs

- Shrinking the growth of your taxable estate

- The joy of gifting

Reducing Future RMDs

Eventually the IRS will make you take Required Minimum Distributions (RMDs) from your retirement accounts. These withdrawals are subject to federal and state ordinary income tax. Thanks to the SECURE 2.0 Act, the starting age for RMDs is now 73 if you were born between 1951-1959, and it increases to 75 if you were born after 1960. Gifting money to your kids today can reduce the size of your retirement accounts. This could lower the tax on your distributions down the road.

Shrinking the Growth of Your Taxable Estate

If you make a monetary gift today, you’ve made sure that those dollars won’t be subject to potential estate taxes later. Not only that, but by moving assets out of your name, you are freezing the value of that gift in the eyes of the IRS. For example, if you give your son $19,000 in 2026, you’ve guaranteed that money won’t grow to $30,000 inside your estate where it could be taxed later. Instead, if your son invests that $19,000, all future growth happens in his name. This allows your family to build wealth faster because the IRS isn’t waiting to take a potential 40% cut at the end of your life.

The Joy of Giving

If you wait to leave your kids or grandkids an inheritance, you never get to see them enjoy your money. Giving money today allows you to watch your adult child buy their first home, help a grandchild graduate debt-free, or enjoy an awesome family vacation while you are still healthy enough to be part of the memories.

First, Make Sure Your Retirement Is Secure

Before you start giving money away, it’s smart to make sure you have a great retirement foundation. You can’t get a loan for retirement, but your children can get a loan for a house, car, or education.

Before you sign that check or transfer those shares, consider if these parts of your retirement plan are in-tune:

- Comfortable & Sustainable Income: You should have a clear understanding of your monthly cash flow. If a major market downturn happened tomorrow, would you still have enough to live on with extra to spare? Ideally, you should be gifting from your excess money, not from the money you need to pay your bills.

- Eliminated High-Interest Debt: It’s hard to justify a monetary gift if you’re still paying 20% interest on a credit card or a high-interest car loan. Be sure to clean up your own balance sheet first so your giving can be sustainable.

- A Solid Long-Term Care (LTC) Plan: This is a big one. According to recent studies by Genworth, the average cost of a private room in an Ohio nursing home can exceed $100,000 per year. Whether you have insurance or you are self-insuring with your own assets, you need a long-term care plan separate from the money you want to give away.

- Emergency Cash: Your roof will probably leak at some point and your car might break down. Before you start a gifting strategy, ask yourself if you have 6–12 months of expenses in a liquid account that is completely separate from the money you intend to give.

Understanding the Gift Tax Rules

You might think that the moment you give your kids money, the IRS is going to show up at your door with a bill. Thankfully, that’s not the case. The IRS has gifting rules, but for most of us, they’re just about tax return paperwork, not actual taxes.

- The Annual Exclusion: Every year, the IRS lets you give a certain amount to as many people as you want, no questions asked. For 2026, that amount is $19,000 per person. If you’re married, you and your spouse can each give $19,000, meaning you can send $38,000 to your son or daughter without any gift tax or even having to report it on your tax return.

- The Lifetime Exemption: What if you want to give more than $19,000 to someone you care about? Let’s say you want to help your daughter with a $50,000 house down payment. You still won’t actually pay taxes out of your pocket if you give her cash. You’ll just need to file a gift tax return (Form 709) to let the IRS know you went over the annual limit. The extra gift amount eats into your lifetime gift and estate tax exemption, which is $15 million in 2026.

- Direct Payments: There is some gray area when it comes to giving money to help with big expenses. For example, if you pay a hospital directly for a family member’s surgery, or pay a college directly for a grandchild’s tuition, that money technically doesn’t count toward your $19,000 exclusion.

Weddings aren’t technically in the unlimited gift legal category like tuition, but there is a smart way to handle them. If you pay the florist, the caterer, or the venue directly, the IRS might view you as the host of the party rather than a gift-giver to your child.

Every family’s situation is different, and tax laws are complicated. Before you start a major gifting strategy, it’s smart to discuss it with your tax professional to make sure you’re reporting everything properly.

Gifting Limits at a Glance for 2026

| Gifting Category | Limit | Tax Filing Required? |

| Annual Exclusion | $19,000 per person | No |

| Annual Exclusion (Married) | $38,000 per household | No* (unless gift-splitting) |

| Direct Tuition / Medical Payments | Unlimited | No |

| Lifetime Exemption (2026) | $15,000,000 | Yes (for gifts over the $19k annual exclusion) |

Simple Ways Retirees Can Gift Money

Sometimes the most impactful way to make financial gifts to your family is also the easiest. If you’ve explored gifting strategies, you may have seen other guides mention complex legal structures like Irrevocable Trusts, UTMA/UGMA custodial accounts, or ways to minimize the Kiddie Tax.

While these instruments have their place in very high-net-worth estates, they can increase the tax noise in your financial plan and, in some cases, create a permanent loss of control. For example, in 2026, your child’s unearned income (like dividends or interest from a gift) above $2,700 is subject to that Kiddie Tax, potentially at your higher tax rate.

I’ve focused this section on direct, low-friction strategies that keep your gifting plan and your retirement in sync, including:

- Cash gifts

- Paying down debt

- Funding major life events

Cash Gifts

As long as you stay under the annual gift tax exclusion of $19,000 per person, you can give cash to your kids and grandkids and don’t have to worry about reporting it to the IRS.

Example: If you have three grandchildren and you want to give each of them $5,000 for the holidays, you can just write the checks. Since each check is under $19,000, these are gift tax free and require no reporting. (The gifts are tax-free assuming you give from bank cash. If you pull the money from your IRA, you might have to pay income taxes.)

Sidenote for grandparents: if your grandchild is applying for college financial aid, a direct cash gift can be seen as ‘untaxed income’ on the FAFSA. This might reduce their need-based financial aid. If they are in their final years of college, this is usually less of a concern, but it’s a detail worth checking out so your gift doesn’t backfire.

Paying Down Debt

Whether it’s student loans or a credit card mess, helping your adult child pay off high-interest debt can make a huge difference in their monthly cash flow and ability to save.

Example: Suppose your son has a $15,000 credit card balance at a 22% interest rate that they racked up during college to stay afloat. If you pay that off for him, you aren’t just giving him $15,000; you’re saving him thousands of dollars in future interest payments and helping his credit score. And because it’s under the annual limit, you won’t need to file a gift tax return.

Funding Major Life Events

This is probably the most common form of giving that comes up with my clients. You want to help pay for your child’s wedding, buy their first car, or help with a down payment on their first home.

When you decide to help with a large purchase like a house, you’ll need to be clear on whether the money is a gift or a loan. If you expect to be paid back, the IRS requires you to charge a minimum interest rate (the Applicable Federal Rate). If you don’t, they may treat the foregone interest as an additional gift. For most of my clients, a clean gift is much simpler and keeps the family harmony intact.

Example: Let’s say you want to help your son with a $30,000 down payment on a house in Dayton, and you are married. You and your spouse can each give him $15,000. Because the total from each of you is under the $19,000 gift tax exclusion, the full $30,000 won’t require filing a gift tax return.

As I mentioned earlier, the IRS sees a direct payment to a car dealer or bank the same as giving cash. That said, when it comes to weddings, if you pay the vendors directly, the IRS might view you as the host rather than a gift-giver. The only other times paying a bill directly is unlimited for gifting is for tuition or medical bills. Be sure to consult your tax advisor if you plan to make a gift.

Summary of Direct Payments

| Expense Type | Direct Payment to Vendor | Filing Status |

| College Tuition | Required | Unlimited (Doesn’t count toward $19k) |

| Medical Bills | Required | Unlimited (Doesn’t count toward $19k) |

| Wedding Costs | Highly Recommended | Possibly Excluded (If viewed as hosting) |

| Cars or Home Down Payments | Required | Counts as a Gift (Subject to $19k limit) |

Tax-Efficient Giving Strategies

If your goal is to support your family while also being mindful of taxes, how you give can be just as important as how much you give. With the right strategy, you can reduce your tax burden while increasing the long-term impact of your gifts.

Here are a few tax-efficient ways to maximize every dollar you pass on:

- 529 College Savings Plans

- Gifting to a “Custodial” Roth IRA

- Gifting Appreciated Assets

529 College Savings Plans

If you are a retired grandparent, you could contribute to your grandkids’ 529 plan. These accounts are great because the money grows tax-free for education. You can even superfund or overfund these accounts by giving five years’ worth of gift exclusions all at once ($95,000 in 2026) without triggering the gift tax.

As an Ohio resident, you get a state tax break just for contributing. For 2026, you can deduct up to $4,000 per year, per 529 beneficiary from your Ohio taxable income. If you are married and filing jointly, that deduction doubles to $8,000 per 529 beneficiary.

Example: If you have two grandchildren and you want to set the tone for their college savings, you and your spouse could contribute $8,000 to each of their 529 plans. Then, you could take a $16,000 deduction towards your Ohio income taxes. If you decided to overfund $95,000 for one grandchild, you could deduct $8,000 this year and carry forward the remaining $87,000 to be deducted in $8,000 increments in future years until it’s all used up.

Gifting to a “Custodial” Roth IRA

If you have a grandchild with a summer job or an adult child just starting their career, you could help them fund a Roth IRA to jumpstart tax-free retirement savings. Since Roth IRAs grow tax-deferred and eventually create tax-free income, you could be giving them decades of compound interest.

To be eligible, your child or grandchild receiving the gift must have earned income (reportable income from a job). You can give them up to the amount they earned that year, or the 2026 limit of $7,500, whichever is less.

Example: If your grandson earns $4,000 working at a camp this summer, you could give him $4,000 to fund a Roth IRA. He gets to keep his summer job paycheck for gas and fun, while you’ve made sure that $4,000 starts growing tax efficiently for his retirement. If that $4,000 sits and grows at an average of 7% for 40 years, it could turn into nearly $60,000 of tax-free retirement wealth.

Gifting Appreciated Assets

This is a slightly more advanced tax move that comes with tradeoffs. If you have stock that’s grown significantly in value, you could give the shares directly to a loved one instead of selling them and giving cash.

When you gift stock, your cost basis (the price you originally paid) carries over to your recipient. If they sell the stock later, they use your original purchase price to calculate their gain. The good news is that they get to use their tax rate, not yours.

Keep in mind that if you hold brokerage account stock until you pass away, your beneficiaries get a ‘step-up’ in basis to the current market value, which wipes out the tax bill entirely. Gifting now makes sense if you want your loved ones to have the money now or if you’re trying to move future growth out of your estate.

Example: Let’s say you bought Apple stock years ago for $2,000 and it’s now worth $15,000. If you sell it, you might owe roughly $2,600 in capital gains taxes (at a 20% rate) before you can give your daughter the remaining $12,400. On the other hand, if you give her the shares directly, she gets the full $15,000. If she’s early in her career and her income is under the 0% capital gains threshold, she could sell the stock and potentially pay $0 in taxes, keeping the full $15,000 for herself.

Common Mistakes Retirees Should Avoid

Before you make a gift, be sure you aren’t accidentally tripping over these common issues:

- Gifting too much, too soon

- Skipping the paperwork

- Medicaid “look-back” issues

- Family inequality

| Potential Mistake | Why it Matters | Idea to Consider |

| Gifting Too Much, Too Soon | It’s hard to un-gift money if you end up needing it later in retirement for healthcare or income. | Your retirement security should come first. Only plan to give what you are 100% sure you won’t need. |

| Skipping the Paperwork | If you give more than $19,000 to one person, the IRS wants to know. | Consult your tax professional and file form 709. You likely won’t owe taxes, but filing keeps you in tune with the IRS. |

| Medicaid “Look-Back” Issues | Ohio reviews every gift you make in the last 5 years before filing for Medicaid. | Want to learn more about gifting issues and Medicaid? Check out my in-depth guide: What Are the Medicaid Rules for Gifting and Long-Term Care? |

| Family Inequality | Giving to one child and not others can create relationship stress and dissonance. | If you help one child with a house, consider telling the others your plan for their inheritance. |

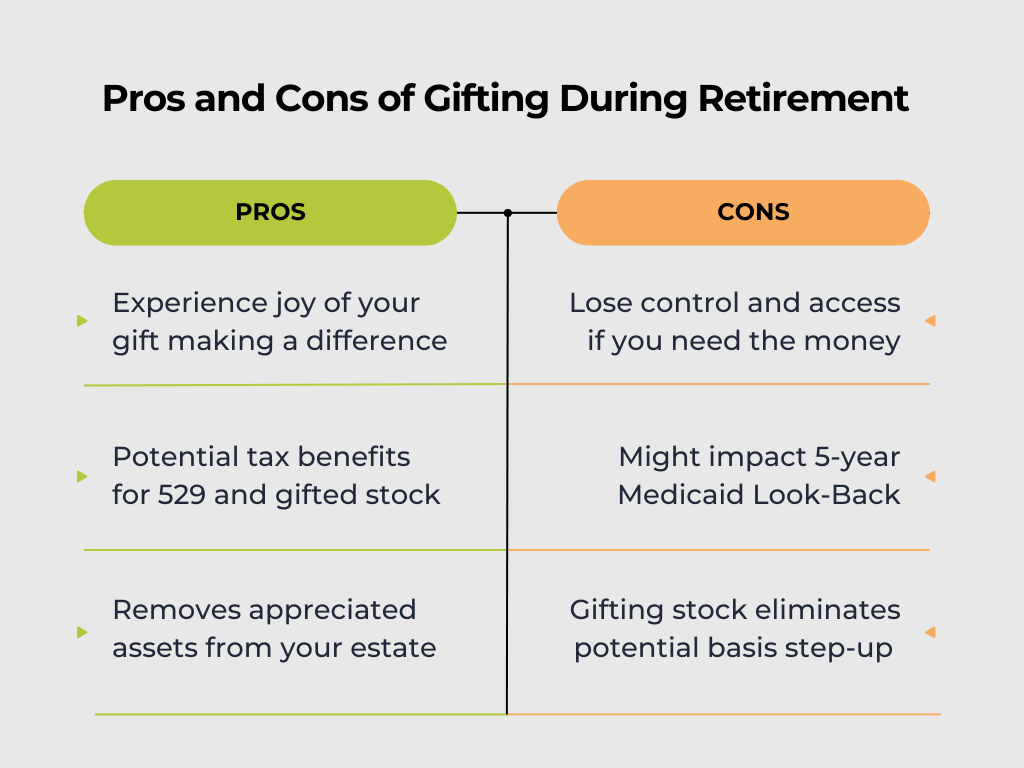

Pros and Cons of Gifting During Retirement

Pros

- You get to experience the joy and impact of your generosity firsthand.

- There can be potential immediate tax benefits, like state tax deductions for 529 contributions or eliminating capital gains on gifted stock.

- Removes future appreciation of assets from your estate tax calculation.

Cons

- You lose control and access of the money you gift in case you need it later on.

- You might accidentally impact your Medicaid eligibility for long-term care support.

- When it comes to gifting brokerage account stock, your beneficiaries won’t receive a ‘step-up’ in basis, meaning they might pay more capital gains tax than if they had inherited your account.

Want More Insight into Your Gifting & Retirement Strategy? Let Stage Ready Financial Planning Help.

If you’re ready to fine-tune your retirement plan and filter out the noise of the financial industry, Stage Ready Financial Planning is here to help.

With the help of your tax professional, we’ll make sure your gifting strategy is in sync with your goals. Stage Ready Financial Planning handles the math so you can enjoy the music. Schedule your intro call today!

Frequently Asked Questions (FAQs)

How much money can I give to my children tax-free in 2026?

For 2026, according to the IRS, the annual gift tax exclusion is $19,000 per person. If you are married, you and your spouse can give a combined $38,000 to each child, grandchild, or any other individual without any tax reporting requirements.

Do I need to file a tax return if I give a gift to my child?

You only need to file a gift tax return (Form 709) if your gift to any one person exceeds the $19,000 annual limit. Even then, you probably won’t owe taxes. The amount you give over $19,000 just gets subtracted from your $15 million lifetime exemption.

Does paying for a grandchild’s tuition count as a taxable gift?

Most likely not, assuming you pay the school directly. Payments made directly to an educational institution for tuition or to a medical provider for healthcare expenses generally don’t count toward your $19,000 annual gift exclusion.

Can gifting money affect my Medicaid eligibility in Ohio?

Potentially yes because Ohio Medicaid has a 5-year “look-back” period. Any gifts you make in the five years before applying for Medicaid can trigger a penalty period that delays your Medicaid benefits. This is true regardless of whether the gifts were tax-free under IRS rules.

Is it better to gift stock or cash?

Gifting appreciated stock can be more tax-efficient if the recipient is in a lower tax bracket, because it allows you to avoid capital gains tax on the growth. That said, gifting stock means the recipient loses the ‘step-up in basis’ they would have received if they inherited the stock after you pass away.

What is superfunding or overfunding a 529 plan?

Superfunding means you get to front-load five years’ worth of gifts into a 529 college savings account at once ($95,000 in 2026) without triggering gift taxes. It can be a great way to move assets out of your estate and secure a state tax deduction in Ohio.

About the Author

Joseph A. Eck, CFP®, is the owner and lead financial advisor at Stage Ready Financial Planning. With a background as a music educator and over a decade as a financial planner, Joseph brings the discipline of a conductor to the complexity of retirement planning and investment management. He specializes in helping Dayton-area retirees “fine-tune” their wealth, ensuring their gifting strategies, tax plans, and investment portfolios are in perfect rhythm with their life goals. Joseph is dedicated to helping clients handle the math so they can focus on enjoying the music of their retirement years. Click here to learn more about Joseph.

Article References

- IRS.gov. “Retirement plan and IRA required minimum distributions FAQs.” Accessed March 9, 2026. https://www.irs.gov/retirement-plans/retirement-plan-and-ira-required-minimum-distributions-faqs

- Charles Schwab. “The Estate Tax and Lifetime Gifting.” Accessed March 9, 2026. https://www.schwab.com/learn/story/estate-tax-and-lifetime-gifting

- Fidelity Investments. “Help reduce estate taxes with lifetime gifting.” Accessed March 9, 2026. https://www.fidelity.com/learning-center/wealth-management-insights/tax-benefits-of-lifetime-gifting

- Genworth/CareScout. “2025 Cost of Care Survey: Ohio Median Annual Costs.” Accessed March 16, 2026. https://www.genworth.com/aging-and-you/finances/cost-of-care.html

- Internal Revenue Service. “Frequently Asked Questions on Gift Taxes.” Accessed March 16, 2026. https://www.irs.gov/businesses/small-businesses-self-employed/frequently-asked-questions-on-gift-taxes

- Morgan Lewis. “IRS Announces Increased Gift and Estate Tax Exemption Amounts for 2026.” Accessed March 16, 2026. https://www.morganlewis.com/pubs/2025/10/irs-announces-increased-gift-and-estate-tax-exemption-amounts-for-2026

- Northwestern Mutual. “Are Wedding Gifts Taxable?” Accessed March 16, 2026. https://www.northwesternmutual.com/life-and-money/are-wedding-gifts-taxable/

- Internal Revenue Service. “Instructions for Form 709: United States Gift (and Generation-Skipping Transfer) Tax Return.” Accessed March 16, 2026. https://www.irs.gov/instructions/i709#en_US_2025_publink100010000

- Ohio House of Representatives. “House Bill 48: Raise Deduction Limits for State 529 Plan and ABLE Savings Account Contributions.” Accessed March 16, 2026. https://www.ohiohouse.gov/news/rep-gross-supports-bill-to-raise-deduction-limits

- TIAA. “How a Roth IRA can give your adult children and grandchildren a running start.” Accessed March 16, 2026. https://www.tiaa.org/public/invest/services/wealth-management/perspectives/roth-ira-for-adult-children

- Charles Schwab. “The Upshot of Gifting Appreciated Stock to Kids.” Written by Hayden Adams. Accessed March 16, 2026. https://www.schwab.com/learn/story/upshot-gifting-appreciated-stock

This communication is for informational purposes only and is not intended as investment, tax, accounting, or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision. Past performance is no indication of future results.