Updated: March 24th, 2026

Are you trying to figure out how much retirement savings you’ll need to live comfortably? The reality is that your answer will vary dramatically based on your particular lifestyle and where you live.

If you’re trying to figure out how much you’ll need in Ohio, the good news is that our affordable cost of living makes retiring comfortably much easier. In this article, we’ll discuss the Ohio-specific budget breakdown you should know to retire and convert your retirement savings into a lasting paycheck.

Key Takeaways

- Ohio’s Cost of Living Advantage is Real: Retiring in Ohio is less expensive than the national average, by about 8% to 12% on average. This is thanks to our much lower median home price (approx. $216,833 vs. $398,000 nationally as of 2026).

- Social Security Gets a Tax Break: Ohio is pretty friendly to retirees as it fully exempts Social Security income from state income tax, and retirees with lower taxable income may owe 0% state income tax initially.

- Go Beyond the 4% Rule: While rules of thumb can offer a ballpark, a customized spending plan that accounts for Ohio’s lower costs, potential tax credits, and adjusting retirement savings withdrawals based on market performance (like the Guyton-Klinger Guardrails) gives you a more confident path to your ideal lifestyle.

Why Retire in Ohio?

Sometimes the midwest gets a bad wrap for its cold winters, but it can be a great place to retire. You can find seasons, a diverse landscape, and an affordable cost of living here. Ohio is a good example, offering a lower cost alternative to the national average retirement.

Affordable Cost of Living

One of the most appealing parts of an Ohio retirement is our low cost of living. A recent study shows that Ohio’s overall cost of living is typically 8% to 12% below the national average. A big driver keeping your annual cost of living low in Ohio is housing. As of January 2026, the National Association of REALTORS® reports that the median price of a home in the U.S. was approximately $398,000. At the same time, the median Ohio home sales price was approximately $216,833, according to Zillow.

Mild Taxes for Retirees

Ohio has a relatively tax-friendly setup for retirees, especially if you rely on Social Security as a core part of your retirement income.

Social Security is Not Taxed

Ohio fully exempts your Social Security retirement income from its state income tax.

Income Tax Brackets

According to the Ohio Department of Taxation, our state has a progressive income tax system with the 2025 top rate at 3.125%. Retirees with taxable retirement income below $26,050 owe no state income tax at all. Also, Ohio’s income tax rate is set to adjust to a flat 2.75% for tax year 2026 and beyond for income over $26,050.

The final 2026 tax rate table has yet to be published, so this is the current chart as of 2025:

| Ohio Taxable Income (Federal AGI) | 2025 Rate |

| $0 – $26,050 | 0% of Ohio taxable nonbusiness income |

| $26,051 – $100,000 | $342.00 + 2.75% of excess over $26,050 |

| $100,001 + | $2,394.32 + 3.125% of excess over $100,000 |

Source: https://tax.ohio.gov/individual/resources/annual-tax-rates

Other Income

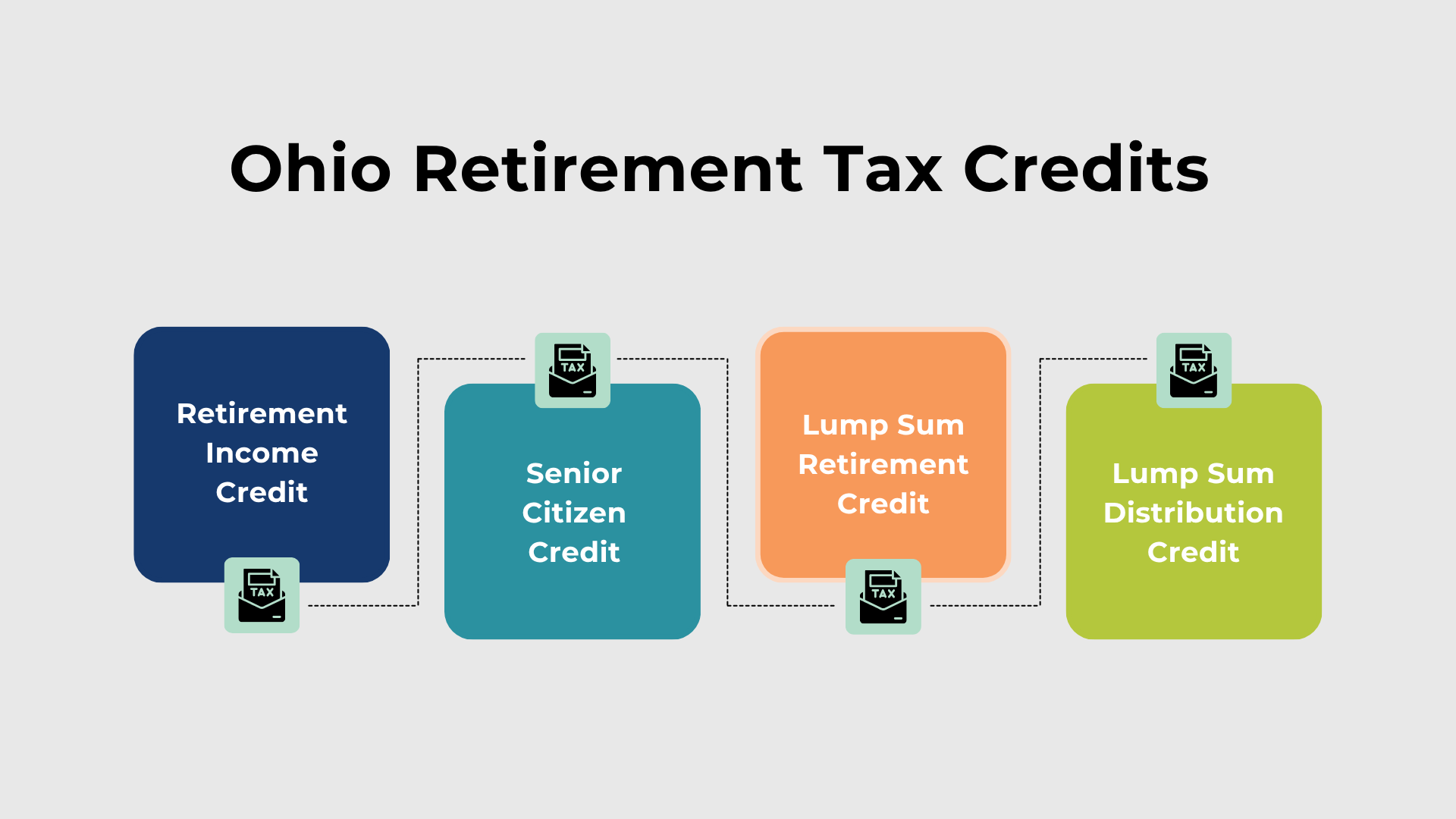

Most pension and pre-tax retirement savings withdrawals are taxed as ordinary income. However, there are credits available for those with lower-to-moderate incomes. Examples include a Retirement Income Credit worth up to $200, and a Senior Citizen Credit of $50 for those 65 and older with Ohio taxable income less than $100,000. For more on this topic, check out our recent blog, Ohio Retirement Tax Strategies to Optimize Your Budget.

Overall Tax Picture

| Category | Facts and Figures |

| Cost of Living | Overall cost is 8-12% below the national average |

| Housing | The median home sale price in Ohio is $216,300 compared to $398,000 nationally |

| State & Local Taxes | The state income tax ranges from 0-2.75% (tax year 2026) and does not apply to Social Security benefits. |

| Property Taxes | Ohio’s average property tax rate is approximately 1.43%, but this is offset by the state’s low cost of housing. |

| Tax Credits | Seniors in lower income brackets may qualify for some state tax credits. |

| Estate & Inheritance Tax | Ohio’s estate tax was repealed on January 1st, 2013, meaning the state does not impose any additional inheritance tax burdens. |

Source: https://stagereadyfp.com/blog/ohio-tax-retirement-strategies/

Among Many Other Benefits

While affordability is a huge draw for retiring in Ohio, the state has a lot more to offer retirees. As a retiree in Ohio, you have access to excellent healthcare. This includes the prestigious Cleveland Clinic and the Ohio State University Wexner Medical Center. Both are consistently ranked among the top hospitals in the United States.

From hiking in Hocking Hills to exploring the art scene in Cincinnati, Ohio offers a wide variety of recreational options. Whether you love the outdoors, sports, or cultural activities, there’s always something to do.

What Does “Comfortable” Retirement Mean?

For my clients in Southern Ohio, “comfortable” usually doesn’t mean a yacht or a luxury villa. It means stability, freedom to enjoy time with the grandkids, and traveling a bit without stressing over the credit card bill.

That said, “comfortable” amounts of income and spending vary greatly from person to person. However you define “comfortable,” you’ll need to make sure your retirement income can easily support it.

Rule of Thumb: 70-80% of Pre-Retirement Income

You’ve probably heard the common guideline that suggests you’ll need to retire with about 70% to 80% of your pre-retirement income to maintain your lifestyle. This percentage helps gauge your target retirement income assuming you spend less when you stop working. It also assumes you can afford to live on less because you’ll have fewer taxes withheld and deductions for retirement savings coming out of your monthly check.

For my clients at Stage Ready Financial Planning, I prefer a more detailed approach: During onboarding, we build a customized retirement spending plan.

- We start by getting a clear picture of how much they spend today.

- Then we layer in healthcare costs, and things like additional travel and fun spending.

- Finally, we inflate these expenses to make sure our clients retirement income will continue to support their cost of living over time.

National vs. Ohio-Specific Averages

According to Nasdaq.com and GoBankingRates, the national average retirement household (age 65+) spends around $57,818/yr, or about $5,000/mo. However, in Ohio, the annual cost is a bit lower. The average retirement expenditure for a retiree here is around $53,308/yr.

$53,308/yr might be your target for a comfortable Ohio retirement. If you plan on more travel or live in a pricier area, you’ll want to budget more.

Ohio Retirement Budget Breakdown

Here is a breakdown of annual cost averages for an Ohio retiree household compared to the national annual cost:

| Expense Category | Average Ohio Annual Cost | Average U.S. Annual Cost |

| Housing | $9,166 | $11,692 |

| Healthcare | $7,640 | $7,540 |

| Groceries and Food | $4,816 | $4,797 |

| Transportation | $4,745 | $4,943 |

| Utilities | $4,151 | $4,236 |

| Other | $22,790 | $24,610 |

| Total | $53,308 | $57,818 |

Note: The “Other” category includes miscellaneous expenses, insurance, entertainment, and discretionary spending. Source: https://www.nasdaq.com/articles/6-reasons-you-need-least-635k-plus-social-security-retire-ohio

Housing

This is probably Ohio’s strongest advantage. Ohio’s housing cost of living is estimated at a whopping 78.4% of the national average. This makes it much easier to pay off your mortgage before you stop working. After that, you’re just on the hook for property taxes, utilities, insurance, and maintenance.

Healthcare

Healthcare is one spot where Ohio is slightly higher than the national average, with a cost index score of 101.2, according to the GoBankingRates data. The good news is that Ohio is home to a couple of the top hospitals in the United States.

Groceries and Food

You might spend close to the national average here, around $4,816/yr. But keep in mind, these figures are just averages. Some households spend over $1,000/mo on groceries and even more on restaurants, while others spend under the state average. Where you shop matters as well as how much protein and organic food you purchase.

Transportation, Utilities, and Miscellaneous Expenses

Costs for transportation and utilities are slightly below the national average retirement spending. That said, one con of retirement in Ohio is that our public transportation system isn’t the strongest. Many cities in Ohio have a local bus service, but we don’t have high-speed rail connecting parts of our major cities or different parts of the state. Ohio also features a lot of rural farmland, so having a car in retirement is usually wise.

How Much Should You Save Based on These Costs?

Once you figure out how much spending you want in retirement, you know your savings must cover some of the annual cost. Remember to factor in your guaranteed income sources like Social Security.

Example: If you think you’ll want to spend $8,000/mo in retirement and you have Social Security and pensions of $4,000/mo, then you know you’ll need to retire with investment income of at least $4,000/mo or $48,000/yr. Based on how aggressively you invest, you can then figure out how much savings you’ll need to generate that income.

How Far Does Social Security Go in Ohio?

According to the Social Security Administration, the average Social Security retirement income is about $24,099/yr, or over $2,008/mo (as of 2025 data). This number is specific to retired workers receiving Social Security benefits and doesn’t factor subtractions for Medicare premiums.

Now let’s look at the average Ohio retiree household annual cost of $53,308:

- Average Annual Cost: $53,308

- Subtract Social Security (Single): −$24,099

- Remaining Income Needed From Retirement Savings: $29,209

Based on this example, $29,209/yr is the income that your savings would need to generate if you wanted to retire successfully in Ohio. In monthly terms, you’d need to draw approximately $2,434/mo from your investments.

Sample Budget: Couple vs. Single

For a couple, if both partners receive average retirement Social Security benefits, that’s over $48,198/yr, covering a decent portion of the Ohio average annual cost ($53,308). This leaves a relatively small gap that your retirement savings need to cover.

For a more “comfortable” lifestyle, let’s bump the annual spending goal up to $70,000 for a married couple. This can account for a bit more travel, dining, and other discretionary fun.

| Scenario | Annual Spending Goal | Less: Estimated Social Security (Couple) | Remaining Annual Income Needed from Savings |

| Comfortable Couple | $70,000 | −$48,198 | $21,802 |

| Comfortable Individual | $70,000 | -$24,099 | $45,901 |

How to Plan Your Savings Goal

Now that you have an idea of the income you need to retire, you’ll need to work backwards to figure out what that means in terms of retirement savings. This is where it pays to work with a financial planner or financial advisor as there are a number of factors that impact how much you can withdraw from your investments sustainably.

That said, to get a ballpark idea, you could apply a simple rule of thumb to calculate how much retirement savings you might need. This shouldn’t be relied on until you speak to a professional and should only be used to help you gauge if you are in the ballpark.

Use the 25x Rule or 4% Rule

There are many different theories and approaches to creating retirement income from your investments. They all depend on how you are invested, your life expectancy, and your spending needs.

The 4% Rule (or 25x Rule), originally made famous by William Bengen are two sides of the same coin.

- The 4% Rule suggests you can withdraw 4% of your total retirement savings in your first year of retirement.

- The 25x Rule simply says you need to retire with 25 times your annual expenses that are not covered by Social Security or a pension.

Using our comfortable couple example that needs to cover $21,802 from their retirement savings:

- Retirement Savings Goal = $21,802 × 25 = $545,050

- Working Backwards = $545,050 x .04 = $21,802

Using our comfortable individual example that needs to cover $45,901 from his/her retirement savings:

- Retirement Savings Goal = $45,901 × 25 = $1,147,525

- Working Backwards = $1,147,525 x .04 = $45,901

Alternatively at Stage Ready Financial Planning, I don’t follow a standard 4% withdrawal rule. I help my Wealth Management clients create income using the Guyton-Klinger Guardrails approach. Usually this means can take a higher distribution rate than 4% if their investments are allocated properly and if we follow the methods suggested as markets fluctuate.

Adjust for Ohio Lifestyle & Inflation

- Inflation: It’s wise to assume that your annual cost of retirement will continue to rise over a 20 to 30-year period of time. For example, inflation in the United States has increased approximately 3% per year on average from 2000-2025. This means you need to plan for your income to continue increasing in retirement.

- Taxes: That $545,050 goal assumes tax-free withdrawals. If a large portion of your investments are in pre-tax accounts (like a Traditional 401(k) or IRA), you’ll likely need to retire with more retirement savings to account for future taxes. This also makes the case for working with a financial planner and tax professional.

Some Tips to Retire Comfortably on Less

If you are worried you’re not on track with your retirement savings, these strategies can help you retire comfortably with a lower cost budget:

Consider Downsizing or Relocating

Just because Ohio has a lower average cost of housing doesn’t mean that your individual home will be cheap. There are many expensive parts of Ohio that can put pressure on your retirement budget.

If your home is your biggest expense, downsizing from a large family home to a smaller, more manageable one is a smart way to reduce costs. You may be able to cut your mortgage, maintenance, property taxes, and utility bills.

The less you need to spend on housing, the less pressure you put on your retirement savings. This directly impacts how much you need to retire with. For more thoughts on the pros and cons of downsizing in retirement, consider exploring our recent blog article: Should I Downsize My Home in Retirement?

Align Your Spending with What Matters

You have more control over your spending in retirement than you might think. There are plenty of ways to reduce or realign your spending if you need to prioritize what really matters to you.

Examples include:

- Shopping around to reduce your utility bills

- Driving less and keeping your vehicles longer

- Annually shop to update your insurance policies including Medicare

- Eat out less, cook more

- Stay healthy to prevent excess medical bills

- Audit your unused subscriptions

- Find free or low cost entertainment

- Pay down high-interest debt

- Save cash for large purchases instead of financing

- Reduce unnecessary bank and investment fees

- Travel smart in the offseason and with senior discounts

- Declutter and sell unused items

- And more…

Take Advantage of Senior Discounts and Tax Credits

Be sure you’re using every tax benefit available to you, especially those that reduce your property taxes and overall cost of living.

The Homestead Exemption

For tax year 2025, Ohio qualifying seniors (age 65+) with an Ohio Adjusted Gross Income (OAGI) under a certain threshold can exempt up to $29,000 of their home’s appraised value from property taxes. Click here to read more.

Ohio Retirement Tax Credits

As mentioned earlier, you may also be able to claim tax credits like the Senior Citizen Credit ($50) and the Retirement Income Credit (up to $200) if your retirement income qualifies.

Is Ohio a Good Place for You to Retire Comfortably?

When it comes to your finances, Ohio is a great place to retire comfortably for the Midwestern saver. A high retirement savings goal can be offset by our affordable cost of living and tax breaks on your Social Security income.

The data shows that if you have saved around $750,000 to $1,000,000 (a median retirement savings amount for the prospective clients we talk to) you are likely well-positioned in the buckeye state. However, your investment portfolio alone is not a plan. For real peace of mind, like knowing your investments are set up correctly and making sure you’re paying the least amount in taxes on your retirement income, consider seeking the help of a financial planner.

Are You on the Right Track for Your Ideal Retirement? Contact Stage Ready Financial Planning Today to Schedule Your Personalized, No-Commitment Consultation

The research and calculations in this article are a great starting point for planning your retirement income. However, they can’t replace a personalized strategy. Your plan needs to account for your specific tax bracket, the mix of funds in your 401(k), and your goals for travel or family expenses.

If you’re over 50, living in Southern Ohio, and have saved $750,000 or more, you’ve earned the right to have confidence with your retirement income. At Stage Ready Financial Planning, my goal is to eliminate your guesswork. Together, we’ll build you a clear, personalized road map that addresses your concerns about taxes and investments. You can stop worrying about the numbers and start living your ideal, comfortable retirement.

Ready to transform your savings into a successful retirement? Schedule your intro call today!

Frequently Asked Questions (FAQs)

How much money do you need to retire comfortably in Ohio?

Data shows that in 2025, the average annual retirement expenses in Ohio are approximately $53,308. Let’s say we increase that figure to $70,000/yr to provide more room for discretionary spending and travel. Based on the need to cover the difference between $70,000 and average Social Security benefits, a couple might need approximately $545,050 in retirement savings (using the 25x rule) to retire comfortably in Ohio.

Alternatively, a single individual with one source of Social Security might need approximately $1,147,525 to retire with $70,000/yr. These numbers are just ballpark calculations. They should be adjusted by a financial planner to account for your asset allocation, risk tolerance, taxes, and inflation.

How much does the average retiree spend in Ohio per year?

Data shows that the average retirement household in Ohio spends approximately $53,308/yr on total living expenses. This figure is lower than the national average of $57,818/yr. These averages include retirees who spend quite a bit more living in Ohio’s pricey neighborhoods, and those who spend much less in lower cost rural areas.

Is $500,000 enough to retire in Ohio?

While $500,000 is a significant amount of retirement savings, it may or may not be enough to retire comfortably in Ohio if it’s your only source of retirement income besides Social Security.

A $500,000 retirement savings balance might provide between $20,000 to $25,000/yr in gross retirement income depending on your asset allocation and strategy. If your Social Security benefits matched the national average of $24,099/yr, your total retirement income could be between $44,099 to 49,099/yr. This range is below Ohio’s $53,308 average retirement cost of living.

As always, these are just averages. Be sure to talk to a professional to nail down the right savings number for your situation.

About the Author

Joseph A. Eck, CFP®, is the owner and lead financial planner at Stage Ready Financial Planning. He’s dedicated to helping retirement savers over 50 in Southern Ohio achieve peace of mind by creating a financial strategy that moves beyond median retirement savings guidelines. With a focus on tax efficiency, investment alignment, and achieving a ‘comfortable’ Midwestern retirement lifestyle, Joseph is committed to providing down-to-earth, professional, fee-only financial guidance. A proud member of the Dayton, Ohio community, he helps couples with $750,000 to $1,000,000+ of retirement savings transform their nest egg into a successful, personalized retirement plan.

Article References

- Nasdaq. “6 Reasons You Need at Least $635K (Plus Social Security) To Retire in Ohio.” Accessed October 27, 2025. https://www.nasdaq.com/articles/6-reasons-you-need-least-635k-plus-social-security-retire-ohio

- GoBankingRates. “6 Reasons You Need $635K (Plus Social Security) To Retire In Ohio.” Accessed October 27, 2025. https://www.gobankingrates.com/retirement/social-security/reasons-need-635k-plus-social-security-retire-ohio/

- RentCafe. “Cost of Living in [Your City, e.g., Dayton], OH 2025 | RentCafe.” Accessed October 27, 2025. https://www.rentcafe.com/cost-of-living-calculator/us/oh/

- Forbes. “Median Home Price By State: How Much Do Houses Cost?” Accessed October 27, 2025. https://www.forbes.com/advisor/mortgages/real-estate/median-home-prices-by-state/

- Ohio Department of Taxation. “Annual Tax Rates.” Accessed October 27, 2025. https://tax.ohio.gov/individual/resources/annual-tax-rates

- Ohio Department of Taxation. “Estate Tax Information.” Accessed October 27, 2025. https://tax.ohio.gov/professional/estate

- Kiplinger. “The 80% Rule of Retirement: Should This Rule be Retired?” Accessed October 27, 2025. https://www.kiplinger.com/retirement/the-80-percent-rule-of-retirement-should-this-rule-be-retired

- Kiplinger. “What Is the Average Social Security Check by Age?” Accessed October 27, 2025. https://www.kiplinger.com/retirement/social-security/average-monthly-social-security-check

- Social Security Administration. “QuickFacts: Statistical Snapshot.” Accessed October 27, 2025. https://www.ssa.gov/policy/docs/quickfacts/stat_snapshot/

- CNBC. “The 4% Rule: How Much Can You Spend in Retirement?” Accessed October 27, 2025. https://www.cnbc.com/2025/09/03/4percent-rule-inflation-retirement.html

- The White Coat Investor. “Comparing Portfolio Withdrawal Strategies in Retirement.” Accessed October 27, 2025. https://www.whitecoatinvestor.com/guyton-klinger-guardrails-approach-for-retirement/

- U.S. Inflation Calculator. “U.S. Inflation Calculator: [Year]→[Year], Department of Labor data.” Accessed October 27, 2025. https://www.usinflationcalculator.com/inflation/current-inflation-rates/

- Ohio Department of Taxation. “Real Property Tax – Homestead Means Testing.” Accessed October 27, 2025. https://tax.ohio.gov/help-center/faqs/real-property-tax-homestead-means-testing/real-property-tax–homestead-means-testing

- Zillow. “United States Housing Market: Median Sale Price by State.” Accessed March 23, 2026. https://www.zillow.com/home-values/

- National Association of REALTORS®. “NAR Existing-Home Sales Report Shows 1.7% Increase in February.” Accessed March 23, 2026. https://www.nar.realtor/newsroom/nar-existing-home-sales-report-shows-1-7-increase-in-february

This communication is for informational purposes only and is not intended as investment, tax, accounting, or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision. Past performance is no indication of future results.