When I’m working with clients, I’m always looking for ways to reduce their lifetime taxes and build resources for healthcare costs. If they have an eligible high-deductible health plan, we’ll probably discuss the benefits of maximizing a health savings account (HSA).

I’m a huge fan of the HSA triple tax benefit. Your contributions lower your income tax bill regardless of how much you make. You can invest the balance, and it compounds tax-deferred. And your withdrawals are tax-free for qualified medical expenses, including Medicare premiums and long-term care costs.

After we’ve discussed the benefits, my clients usually ask: “Can you contribute to an HSA after retirement?”

In this article, we’ll look at how you contribute to an HSA as you approach age 65 and beyond. We’ll discuss the rules you need to know to keep your savings in sync with the IRS and avoid penalties.

Key Takeaways

- Medicare Ends Contributions: Turning 65 doesn’t halt your HSA contribution eligibility, but enrolling in Medicare does.

- 6 Month Backdating: If you delay Medicare to work past 65 at a large company, you’ll need to stop making HSA contributions six months before you enroll in Medicare to avoid tax penalties.

- Age 65 Flexibility: At 65, the IRS removes the 20% non-medical withdrawal penalty, allowing your HSA to function just like your Traditional IRA.

Can You Contribute to an HSA After Retirement?

You might be surprised to learn that you don’t have to stop making HSA contributions when you retire or turn 65. Unlike your traditional IRA or a 401(k), HSA contributions aren’t dependent on having earned income. You can fund your account using bank cash and your HSA doesn’t have to be connected to an employer.

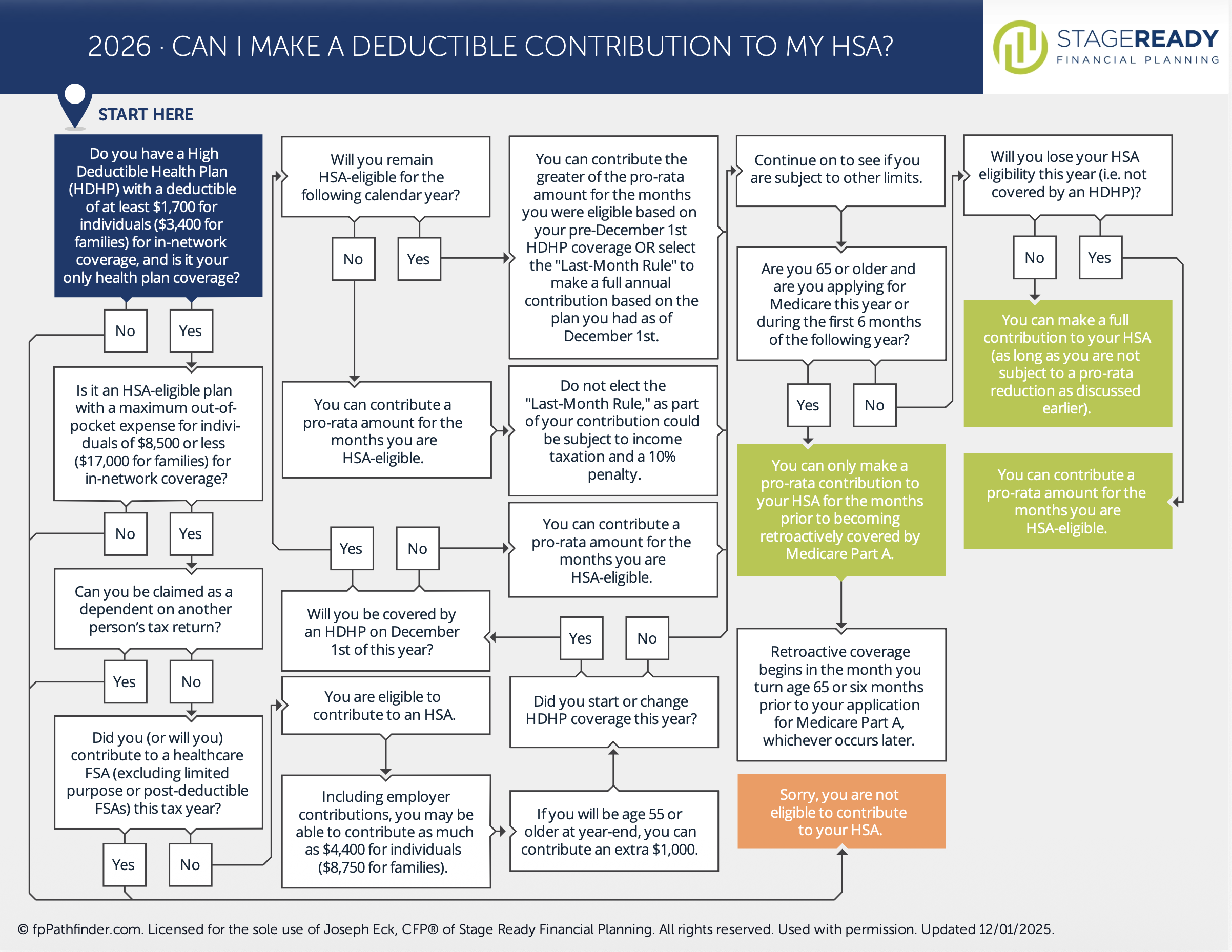

Instead, if you want to put money in an HSA, you’ll need to be enrolled in an eligible high deductible health plan and have no other disqualifying health coverage. According to IRS Publication 969, enrolling in any part of Medicare is what officially ends your eligibility. So if you retire before you need those government benefits, you still have some time to add to your account and build a tax-free bucket for future medical expenses.

HSA Eligibility Rules in Retirement

If you want to contribute to an HSA in retirement, there are some IRS rules you’ll need to follow:

- Maintain coverage with an eligible high deductible health plan: For 2026, the IRS says that your health plan must have a minimum annual deductible of $1,700 for self coverage or $3,400 for a family policy. Your maximum out-of-pocket expenses also can’t exceed $8,500 for self or $17,000 for families.

- Can’t have other disqualifying health coverage: You’re not allowed to simultaneously enroll in a traditional low-deductible health insurance plan, a spouse’s non-HDHP, or a flexible spending account (FSA) that covers the same medical expenses.

- Not being enrolled in Medicare: Age 65 doesn’t stop you, but Medicare enrollment ends your ability to make HSA contributions.

- You can’t be claimed as a dependent: You aren’t eligible to make HSA contributions if you are claimed as a dependent on someone else’s tax return.

Can You Contribute to an HSA After Age 65?

If you want to keep adding to your HSA after 65, you’ll need to keep employer health coverage so that you can decline signing up for Medicare. You’ll also need to check the size of your company.

According to AARP, if your employer has 20 or more employees, you’re probably in good shape. The company must offer you the exact same HDHP health plan options as all other employees and they can’t force you onto Medicare.

But if you work for a small business with fewer than 20 employees, the rules are different. Small employers are allowed to mandate that you transition to government coverage. They can modify your employer policy so that Medicare becomes the primary payer. If you don’t sign up for Medicare at age 65, your employer’s health plan can refuse to pay your medical bills.

Example: Let’s consider two neighbors, both turning 65 this year. They’re both still working and enrolled in a high deductible health plan.

- Neighbor A works as an engineer for a manufacturing company with 75 employees. Because they have more than 20 workers, he can decline all parts of Medicare, keep his employer’s HDHP, and continue to contribute to his HSA past age 65.

- Neighbor B is a mechanic working for an independent auto shop with only 8 employees. His employer has fewer than 20 workers and his health insurance plan states that Medicare becomes the primary payer at age 65. If Neighbor B declines Medicare enrollment, the small business plan won’t pay his claims. He’s basically forced onto Medicare, which halts HSA contributions and could mean tax penalties.

Why Medicare Stops HSA Contributions

You might be wondering why Medicare coverage stops you from adding to your HSA. The biggest reason is that it doesn’t meet the definition of a high deductible health plan. Here’s a look at how the 2026 Medicare coverages contrast with the HSA guidelines:

- Medicare Part B Deductible: According to Medicare.gov, the 2026 Medicare Part B deductible is $283/yr. To make an HSA contribution, the IRS says that your health plan needs to have a deductible of at least $1,700 for single coverage or $3,400 for a family policy.

- Out-of-Pocket Maximum: Another HSA rule is that your health insurance plan must cap your max out-of-pocket expenses at $8,500/yr for single coverage or $17,000/yr for your family. Medicare Parts A and B have no out-of-pocket maximums. Your 20% co-insurance under Part B can continue indefinitely.

IRS rules also state that you’re not allowed to hold any form of secondary health insurance that doesn’t qualify as a HDHP. If you’re still employed with a high deductible plan, and you enroll in Medicare Part A, the IRS counts this as ineligible secondary coverage, so you can’t add to your HSA.

HSA Contribution Limits (If You’re Still Eligible)

If you’re allowed, here’s what you can contribute to your health savings account for 2026:

| Coverage Type | Standard | Age 55+ Catch-Up | Total Possible |

| Self-Only | $4,400 | $1,000 | $5,400 |

| Family Policy | $8,750 | $1,000/spouse** | $9,750 – $10,750 |

* https://www.irs.gov/publications/p969

** As a married couple over age 55, you can save an extra $2,000 total. But the rules state that you can’t put both catch-up amounts into a single account. You’ll have to put $1,000 into your HSA and your spouse will need to put $1,000 into their own separate account.

Common Scenarios (What Applies To You?)

Let’s look at how these rules play out in different situations and how you can maximize your HSA contributions for as long as possible, including:

- Retire before 65 (no Medicare yet)

- Retired and enrolled in Medicare

- Working past 65 and delaying Medicare

Retired Before 65 (No Medicare Yet)

If you retire before 65, you can start using your HSA to pay for medical expenses or you can keep contributing as long as you have an eligible high deductible health plan. It doesn’t matter if it’s your spouse’s policy, a private health plan, or COBRA coverage. Because HSA contributions aren’t tied to income limits, many of my retired clients will use them to lower their annual tax bill.

Example: John and Susan retire at age 62. They’ve built a strong nest egg and are bridging the gap to Medicare by purchasing an eligible HDHP health plan on the ACA marketplace. As long as they keep qualifying coverage throughout the year, the IRS lets them make full HSA contributions plus a $1,000 catch-up per person. In 2026, they’ll reduce their taxable income by $10,750 and pad their future tax-free investments.

Retired and Enrolled in Medicare

Even if you’re enrolled in Medicare, you can still maximize your HSA strategy by staying invested and making strategic distributions. You might decide to use your account to cover expensive premiums and out-of-pocket costs instead of drawing from your IRAs to keep your tax bill lower. You could also let your balance grow and compound for larger medical costs later in retirement like long-term care.

Example: David fully retires at age 66 and enrolls in Medicare Parts A and B. He stops making new HSA contributions to avoid IRS penalties. He decides to cover his current medical expenses out of pocket so his health savings account can grow and be used for emergencies or long-term care.

Working Past 65 and Delaying Medicare

If you’re 65, you can keep contributing to your HSA and lowering taxes by staying on your large employer’s high deductible health plan. But you’ll have to decline all parts of Medicare including the free Part A. Keep in mind that when you stop working and apply for Medicare, your coverage automatically backdates six months. So if you want to avoid IRS tax penalties, you’ll have to tell payroll to halt HSA contributions six full months before you sign up.

Example: Sarah turns 65 but decides to keep working for her company, which has around 100 employees. She keeps her HDHP and declines Medicare Part A and Part B so she can continue making HSA contributions. At 67, she decides to finally retire. She schedules her Medicare enrollment to begin in October. To prevent tax penalties, Sarah stops HSA payroll contributions in March.

What Happens If You Contribute After You’re No Longer Eligible?

If you put money in an HSA when you aren’t allowed, your excess contributions are subject to a 6% tax penalty for every year they stay in your account. So it’s best to get them out as quickly as possible.

You can avoid tax penalties for ineligible contributions if you reverse them before the tax filing deadline. When you reverse HSA contributions, the dollars you put in plus their earnings will need to come out. The reversed earnings will count as income that you’ll have to pay tax on. If you forget to reverse them in time, you’ll calculate your penalty by completing IRS Form 5329.

Example: Mark transitions to Medicare in July, meaning he’s only eligible for the first 6 months of the year. He forgets and ends up contributing $4,000 to his HSA by December. Based on 6 months of eligibility, his contribution limit was $2,200, leaving him with an $1,800 excess contribution.

If Mark does nothing, the IRS will hit him with a $108 penalty (6% of $1,800) on Form 5329 every year it sits there. To fix it, Mark contacts his HSA administrator before April 15th and requests an excess contribution removal. They send him a check for the $1,800 plus $50 in investment growth. Mark adds the $1,800 back to his taxable income, pays income tax on the $50 earnings, and avoids the 6% penalty.

Can You Still Use Your HSA After Retirement?

You absolutely can. Even though you can’t contribute once you’re on Medicare, the money you’ve saved is yours.

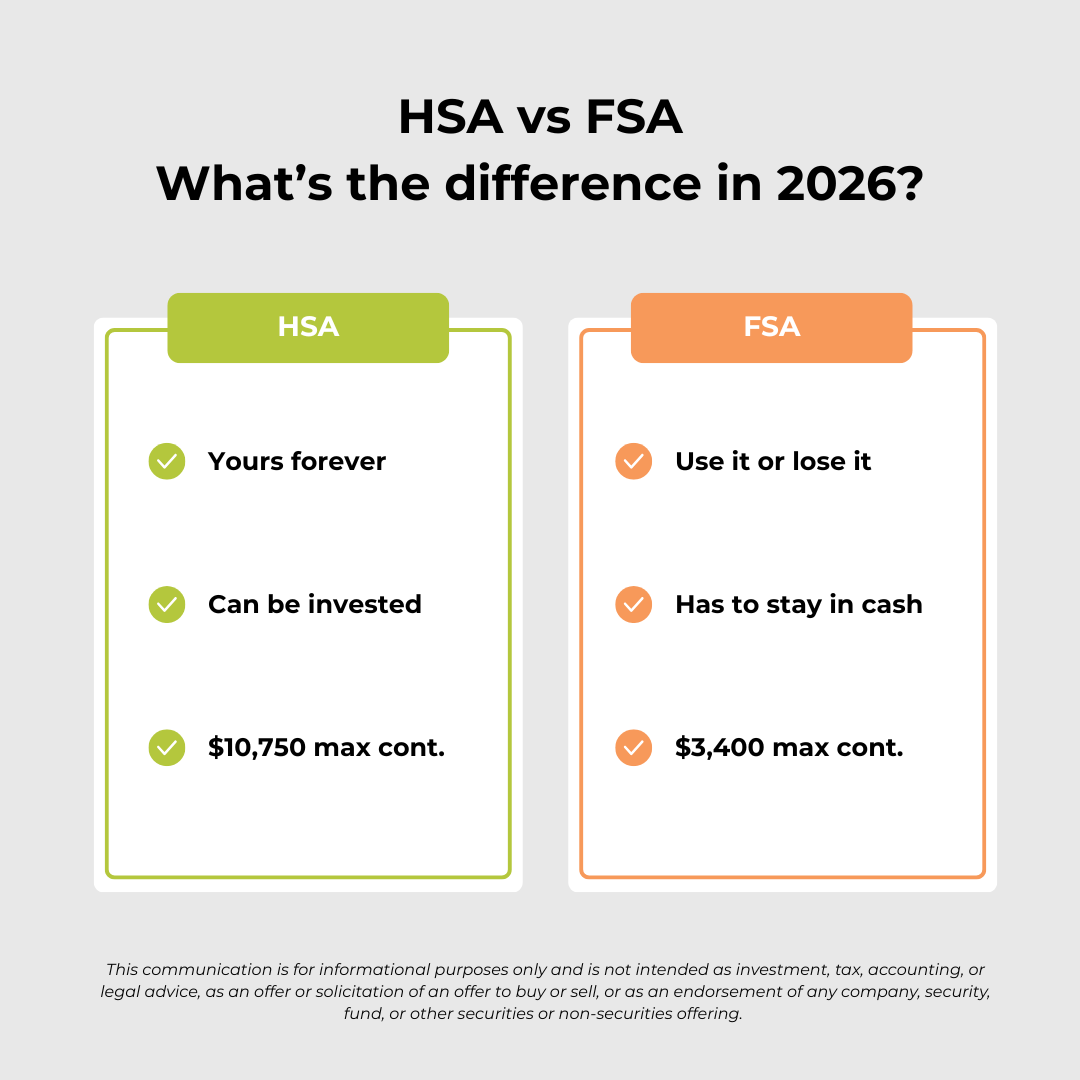

I’ve noticed that retirement savers tend to confuse the rules around HSAs with Flexible Spending Accounts (FSAs), but they’re very different vehicles:

- FSA: These accounts require you to spend your money down by the end of the year or forfeit the remainder.

- HSA: There’s no use-it-or-lose-it rule. Your account value carries over each year, stays invested, and can be used throughout retirement.

Spending Your Tax-Free Dollars

You can pull money from your HSA tax-free at any age to pay for qualified medical expenses. In retirement, this includes your deductibles, copays, hearing aids, dental work, and monthly Medicare premiums. You can also use your HSA to pay for hospital bills and long-term care costs.

Age 65 Flexibility

While it’s probably best to use your HSA for medical expenses, once you turn 65, the IRS removes the 20% penalty for non-medical withdrawals. This means you can take penalty-free withdrawals to buy a camper or pay for a vacation. You’ll just have to pay income tax on any money you take out. At 65, your account functions just like your Traditional IRA.

Want More Retirement Planning Help? Schedule Your No-Commitment, No-Hassle Consultation Today

If you’ve saved at least $750,000 for retirement, you’ve done the hard work. Now, it’s time to make sure all your financial instruments are in sync with your ideal retirement. Stage Ready Financial Planning specializes in helping savers over 50 reduce the noise of planning complexity and taxes.

I’ll help you maximize your health savings account in coordination with Medicare enrollment so that you have the tax-free resources you need to enjoy a confident retirement. I’ll handle the math so you can enjoy the music. Schedule your complimentary intro call today!

Frequently Asked Questions (FAQs)

What counts as a qualified medical expense for HSA withdrawals?

The IRS lets you make tax-free HSA withdrawals to pay for dental care, vision expenses, hearing aids, prescription drugs, doctor copays, and hospital stays. In retirement, it also covers your out-of-pocket Medicare premiums, and a portion of tax-qualified long-term care insurance premiums based on your age. You can even use your HSA to pay for in-home care or long-term care costs later in life. For the full list of qualified medical expenses, be sure to consult IRS Publication 969.

Can I use my retirement HSA to pay for a spouse’s medical costs?

You can. As long as you’re married, you can use your HSA to pay for your spouse’s qualified medical expenses tax-free. Regardless of age, this rule applies even if your spouse is enrolled in Medicare or has separate health insurance.

Does my HSA have Required Minimum Distributions (RMDs)?

Good news: unlike your Traditional IRA and 401(k), your HSA does not have mandatory distributions. The IRS won’t force you to take money out to pay taxes at a certain age because your account was designed to be used tax-free for medical expenses. You can keep your HSA invested for as long as you live.

What happens to my HSA if I pass away?

If you’re married and your spouse is the primary beneficiary, your HSA can transfer tax-free to them when you pass away. Your HSA becomes theirs and continues to work under the same tax rules. According to IRS Publication 969, if you name anyone else as beneficiary (child, grandchild, etc) the account stops being an HSA. Your entire balance becomes taxable to them in the year of your passing.

About Joseph Eck, CFP®

Joseph A. Eck, CFP®, is the owner and lead financial advisor at Stage Ready Financial Planning. He’s built his practice to help retirement savers over 50 achieve confidence by orchestrating their ideal retirement plan. Joseph provides down-to-earth, fiduciary guidance on how to navigate complex retirement transitions, including synchronizing HSA contributions with Medicare enrollment, reducing lifetime income tax, and optimizing your investments to match your ideal lifestyle. As a former educator and active member of the Dayton, Ohio community, Joseph brings the discipline and clarity of a conductor to the complexity of wealth management. Click here to learn more about Joe.

About Stage Ready Financial Planning

Stage Ready Financial Planning helps retirees and savers over 50 throughout Dayton and Southwest Ohio stay in sync with their goals through fee-only financial planning and fiduciary wealth management. Designed for households with $750,000+ invested for retirement, Joseph Eck, CFP® helps clients coordinate retirement income, investments, taxes, and more into one cohesive strategy.

From orchestrating predictable retirement income to reducing unnecessary taxes and market “noise,” Stage Ready Financial Planning was built to help clients enjoy retirement with clarity, confidence, and financial harmony.

Article References

- Internal Revenue Service. “Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans.” Accessed June 8, 2026. https://www.irs.gov/publications/p969

- AARP. ”Still Working at 65? When Do You Sign Up for Medicare?” Accessed June 8, 2026. https://www.aarp.org/medicare/do-i-enroll-in-medicare-age-65-even-if-still-working/

- Medicare.gov. “Costs: What Medicare Covers and What You Pay.” Accessed June 15, 2026. https://www.medicare.gov/basics/costs/medicare-costs

- Centers for Medicare & Medicaid Services. “Medicare Enrollment and Rules for HSA Contributors.” Accessed June 8, 2026. https://www.cms.gov

- Internal Revenue Service. “Instructions for Form 5329: Additional Taxes on Qualified Plans and Other Tax-Favored Accounts.” Accessed June 15, 2026. https://www.irs.gov/pub/irs-pdf/f5329.pdf

- fpPathfinder. “2026 Can I Make a Deductible Contribution to My HSA?” Checklist licensed for Stage Ready Financial Planning. Accessed June 15, 2026.

This communication is for informational purposes only and is not intended as investment, tax, accounting, or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision. Past performance is no indication of future results.