A brokerage account is a great instrument for distributing tax efficient income in the early years of retirement. It can help you bridge the gap between your working years and Social Security or IRA distributions.

But when it comes to managing your brokerage account in retirement, your approach will require some knowledge and planning. Because without a clear strategy for trading and income, even small brokerage account mistakes can disrupt your income and leave you paying the IRS more.

In my experience as a CFP® professional and even drawing from my background in music conducting, I’ve found that a retirement plan requires the same ‘rhythmic precision’ as an ensemble. One mistimed withdrawal is like a missed beat; it can throw the entire performance out of sync.

In this article, we’ll discuss the common pitfalls that create dissonance in your brokerage account so you can fine-tune your investment strategy and keep your retirement performance on track.

Key Takeaways: Brokerage Mistakes and Fixes

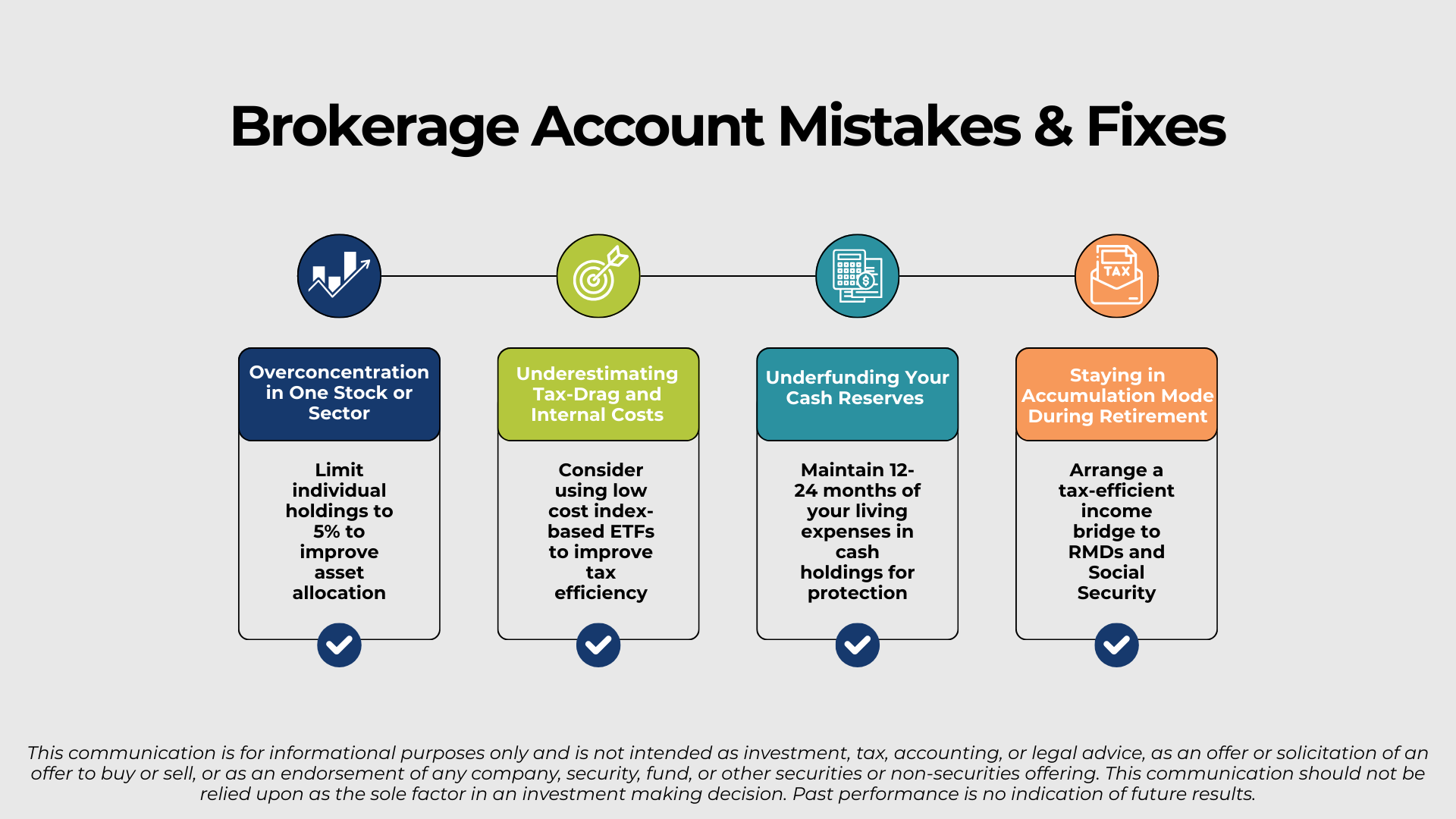

- Overconcentration in single stocks

- The Fix: Limit individual holdings to 5% to improve asset allocation discipline.

- High “Tax Drag” and expense ratios from active funds

- The Fix: Transition to tax-aware, index-based ETFs to keep more of your returns.

- Underfunding your cash reserves

- The Fix: Maintain 12–24 months of spending in a liquid buffer to avoid selling in a down market.

- Staying in “Accumulation Mode”

- The Fix: Arrange a “Tax-Efficient Income Bridge” to protect your IRAs and 401(k)s.

Why Brokerage Account Mistakes Matter More in Retirement

While you were working, time was on your side. If the market dropped, you had years of paychecks to fall back on. Your steady contributions were purchasing shares at lower prices while the market was on sale.

In retirement, the rules change. Your accounts are now your primary liquidity source and mistakes don’t just affect your balance. They impact your ability to sustain your lifestyle. Investing involves risk, and those risks become more intense when you’re living off of your assets. For example, selling investments at a loss early in retirement can create “sequence of returns” risk, permanently reducing the longevity of your portfolio.

Also, without a disciplined investment strategy, “tax drag” from inefficient assets can spike your bill and dampen your returns. Also, realizing large capital gains or receiving significant ordinary dividend distributions can push up your Modified Adjusted Gross Income (MAGI). You might accidentally trigger Income-Related Monthly Adjustment Amount (IRMAA), meaning you’ll have to pay more for Medicare.

What Are 4 Brokerage Account Mistakes Retirees Should Know About?

1. Overconcentration in One Stock or Sector

Unlike the pre-set menu of investments in your 401(k), a brokerage account allows you to buy any of the household names you hear about in the news. But freedom comes with tradeoffs. The risk in having unlimited investment choices is that it could lead to a lack of asset allocation discipline. If you aren’t careful you could throw off your asset allocation from the target that aligns with your financial objectives and risk tolerance.

Individual stock prices are far more prone to volatile markets than broader market indexes and even the most established blue-chip companies can experience a sudden large dip. If it happens at the wrong time in retirement, it could impact your ability to sustain your retirement income.

Overconcentration can also happen silently. You might hold a large position in a tech stock like Microsoft, while also owning a ‘cap-weighted’ S&P 500 ETF where that same stock is a top holding. This ‘hidden overlap’ can leave you more exposed to a single company’s volatility than your asset allocation suggests.

Example:

Consider Bill, a retiree in Hamilton, OH who decided to keep a significant portion of his brokerage account in General Electric (GE) about a decade ago. At the time, GE was considered an icon of corporate stability and a “safe” dividend play for retirees.

However, starting in 2017, the company started to struggle. In that year alone, GE’s stock plummeted 44.8%. By the end of 2018, the stock was trading at roughly $7.30 per share, down more than 58% for that year. It was eventually ejected from the Dow Jones Industrial Average. To make matters worse for retirees like Bill, GE slashed its quarterly dividend from $0.24 to $0.12 in 2017, and then slashed it again to just a penny in late 2018.

Because Bill was overconcentrated in this one financial instrument, his financial plan hit a major roadblock. He didn’t just lose principal; his monthly income rhythm was shattered right when he needed it most.

2. Underestimating “Tax Drag” and Internal Costs

In the past, investors worried about paying $50 commissions to buy or sell a stock. Today, most major platforms offer commission-free trading, making it feel like your brokerage account is free to operate. But this is a misconception because the real cost of owning a brokerage account isn’t the fee you see on your monthly statement. It’s the silent leak of taxes and internal fund expenses.

“Tax drag” is the reduction in your net return caused by the taxes you pay on dividends, interest, and capital gains distributions. It’s not always easy to detect because you pay those taxes out of your bank account in April, rather than seeing it deducted directly from your portfolio.

According to Morningstar, the average actively managed mutual fund can experience tax drag in excess of 1% per year. To put that in perspective, in 2024, roughly 78% of mutual funds paid out a taxable capital gain, compared to only about 7% of ETFs. When you combine that tax hit with a higher internal expense ratio, you could be losing a massive portion of your performance without ever realizing it.

Financial advisors often refer to the value added by tax-efficient strategies as ‘Tax Alpha.’ It is the measurable outperformance your portfolio gains simply by reducing the IRS’s cut. Research by Schwab suggests that a disciplined tax-aware strategy can add up to 1.1% in annual returns over a buy-and-hold approach.

To keep your retirement income at its highest volume, your investment strategy should likely favor “tax-aware” instruments like low cost index-based ETFs with lower turnover ratios. This means the fund manager is buying or selling less on a regular basis. For the bond portion of your brokerage account, consider using municipal bond ETFs because they offer interest income that is generally exempt from federal taxes.

Example:

Meet Robert, a retiree in Beavercreek, Ohio. He has $500,000 in a brokerage account invested in a top-rated active mutual fund he’s held since the late 1990’s. The fund has an expense ratio of 0.85% and a high turnover rate.

On paper, the fund returned 8% this year. But because of the high turnover, the fund distributed significant capital gains, creating a “tax drag” of 1.2%. Between the expense ratio and the tax hit, Robert’s real-world return was actually closer to 5.95% before even considering inflation.

Over 10 years, that 2% difference could cost Robert over $140,000 in lost growth. By not understanding the tax ramifications of his investment choices, Robert is essentially paying a silent tax that could be more expensive than hiring an advisor.

3. Underfunding Your Cash Reserves

One of the most common stressors I see with my retired clients is being forced to sell equity securities during a down market. In the financial world, we call this “sequence of returns” risk, but for you, it probably feels like watching your hard-earned savings evaporate.

The risk of underfunding your cash reserve isn’t just about paying taxes; it’s about avoiding the ‘behavioral gap.’ According to Fidelity, an investor who missed just the five best days in the market over a 30-year period could see their long-term gains reduced by as much as 37%. Your cash buffer ensures you never have to ‘exit’ at the wrong time.

To prevent this, I regularly recommend maintaining a healthy cash bucket in retirement. This usually looks like at least 12 to 24 months of your spending kept in stable, liquid accounts like high-yield savings or money market funds. Your cash acts as a buffer, ensuring your long-term investments have the time they need to recover from market volatility.

But with a brokerage account, there’s a secondary benefit to holding cash that many retirees overlook: rebalancing and tax efficiency. A fully invested brokerage account makes rebalancing difficult. Any move you make requires selling something, which potentially triggers capital gains taxes. If you keep a healthy cash reserve, you can rebalance by using your cash to buy underweighted assets rather than being forced to sell things that have unrealized gains.

Example:

George is a retiree in Centerville, Ohio. He has close to $1 million in his brokerage account with an asset allocation of 60% stocks and 40% bonds. He keeps $0 in cash, choosing to be fully invested.

When the stock market has a great year, his stocks grow to 70% of his portfolio. To get back to his 60/40 orchestration, George has to sell $100,000 worth of stock. Because it’s a taxable account, that sale triggers a $15,000 tax bill (assuming a 15% long-term capital gains rate). If his total income is high enough, he might even owe an additional 3.8% in Net Investment Income Tax (NIIT).

If George had maintained a cash reserve, he could have used his Social Security checks and some of that liquid money to buy bonds over the year, gradually nudging his portfolio back in sync without creating a taxable sale. By being too invested, George accidentally turned a routine portfolio adjustment into a mandatory encore for the IRS.

4. Treating Your Brokerage Account Like an Accumulation Instrument in Retirement

I regularly talk to retirees that keep their brokerage account in the same growth mode they used while they were working. As a saver, a market dip is just a discount on your statements but in retirement, it’s a risk to the longevity of your income. If your account is too aggressive, you might be forced to sell stocks while they are down, triggering “sequence of returns” risk.

As I discussed in my previous article on withdrawal strategies, the arrangement of your withdrawals makes a big difference and a well-managed brokerage account can serve as your tax-efficient income bridge to RMDs and Social Security.

In 2026, married couples can have a taxable income up to $98,900 and still qualify for a 0% federal tax rate on long-term capital gains. If you take distributions from your brokerage account first, you’ll only pay capital gains tax on the profit, allowing your tax-deferred IRAs to continue growing undisturbed. This approach might keep your taxable income lower in the early years of retirement.

Example:

Sarah is retired in Kettering, Ohio, and has $300,000 in a brokerage account that is still 90% invested in high-growth tech stocks. This is the same allocation she used 10 years ago and she plans to wait until age 70 to claim Social Security to maximize her benefit.

In her first year of retirement, the tech sector falls 20%. Because her account is too aggressive and she has very few conservative investments, she is forced to sell those tech shares at a massive loss just to cover her property taxes and travel.

If Sarah had shifted her asset allocation to be more income-ready, she could have used the brokerage account to “bridge the gap” to age 70 with much less stress. By treating her retirement like the accumulation phase, she accidentally sold low and turned a temporary market dip into a permanent loss of retirement income.

How Retirees Can Avoid These Mistakes

Here are 4 ways that you can improve your brokerage account investment strategy and financial plan:

- Rebalance with Cash, Not Sales: Instead of selling appreciated stocks and triggering taxes, use your dividends, interest, and cash bucket to buy underweighted investments. This is the cleanest way to avoid unnecessary capital gains taxes.

- Audit Your Tax Efficiency: Review your holdings for tax drag. If you have old mutual funds with high internal costs and turnover, look for opportunities to transition into index-based ETFs. In years where the market is down, you can use tax-loss harvesting to move into these more efficient vehicles. Just be careful to avoid a “Wash Sale” by buying a “substantially identical” security within 30 days.

- Build a Buffer: Try to avoid putting yourself in a position where you have to sell equities in a market dip. Consider keeping at least 12 to 24 months of your monthly spending in a money market fund so that your long-term growth has the “quiet” it needs to recover from market volatility.

- Coordinate Your Withdrawal Order: Consider treating your brokerage account as your income bridge in the early years of retirement. By spending down taxable assets first, you keep your IRAs growing tax-deferred and can potentially stay in a 0% or 15% capital gains bracket before RMDs begin. In 2026, married couples can have a taxable income of up to $98,900 and still pay $0 in federal capital gains tax.

Pros & Cons of Self-Managing a Brokerage Account

| Pros | Cons |

| Direct Control: You have total authority over the timing of every trade and withdrawal. | Emotional Dissonance: It’s difficult to remain objective when your grocery money is at risk during a 20% market drop. |

| Fee Savings: You avoid paying for professional management on your assets. | Hidden Tax Bills: Without technical expertise in tax-loss harvesting or lot-selection, you might lose more to the IRS than you would have paid an advisor. |

| Personal Interest: If you enjoy the research, managing your own investments can be an interesting project. | Complexity Overload: Managing the “Wash Sale” rule or coordinating withdrawals to avoid NIIT surcharges requires constant monitoring and expertise. |

Final Thoughts

A brokerage account is one of the most versatile instruments in your retirement arrangement. If it’s used correctly, it provides a tax-efficient income bridge before RMDs and Social Security kick in, protecting your IRAs and helping you keep more of your hard-earned money.

But as we’ve discussed, a few mistakes like unnecessary tax drag, overconcentration, or a lack of cash reserves can quickly disrupt your income and reduce the likelihood that your investments last as long as you do.

Quick Review: Is Your Brokerage Account Out of Tune?

- Does any one stock or sector represent more than 5% of your total portfolio?

- Are you still holding active mutual funds that trigger “phantom” capital gains every December?

- Do you have 12–24 months of spending in a liquid money market fund to avoid selling in a dip?

- Are you strategically using taxable assets for income in early retirement to potentially qualify for the 0% or 15% capital gains rate?

Looking to Avoid Mistakes Like This and More for Your Retirement? Let Stage Ready Financial Planning Help You

If you’re over age 50 and have built a portfolio of $750,000 or more, you’ve already mastered the accumulation stage. Now, you probably want to make sure that your investment strategy is optimized for income.

Stage Ready Financial Planning specializes in helping families across Southwest Ohio navigate this exact transition. While this article outlines common pitfalls, a fee-only financial advisor like myself can provide the personalized tax-loss harvesting, asset allocation, and withdrawal strategies required to protect your hard-earned savings.

I’m here to help you manage the technical logistics of your brokerage account and build a reliable income bridge so you can focus on enjoying the retirement lifestyle you’ve spent decades building.

Schedule your intro call today!

Frequently Asked Questions (FAQs)

Is it risky to manage a brokerage account in retirement?

It can be, but it really depends on your experience, knowledge, and approach. While it’s easy to be aggressive when you’re working, it’s much harder to stay emotionally disciplined when a 20% market drop affects your actual grocery money. Self-managing a brokerage account also requires a certain level of expertise to avoid “Wash Sales,” owning tax-inefficient investments, and accidentally triggering a higher tax bracket.

How should retirees use a taxable brokerage account for income?

Your brokerage account is a great instrument to use for income in early retirement before RMDs and Social Security kick in. You can allow your IRAs to grow tax-deferred longer and potentially stay in the 0% or 15% capital gains bracket.

How are brokerage accounts taxed in retirement?

Unlike your IRA, transactions in a brokerage account are taxed each year. You’ll owe the IRS for any interest, dividends, and realized capital gains. If you aren’t careful, “tax drag” from inefficient investments (like high-turnover mutual funds) can trigger these taxes even in years when you didn’t sell anything.

Do retirees pay capital gains taxes on brokerage account withdrawals?

In a brokerage account, you’ll pay tax on the gain of the asset sold, not the total withdrawal amount. For example, if you sell $10,000 worth of stock but your original “basis” (purchase price) was $8,000, you’ll be taxed on that $2,000 profit. Your specific tax rate will depend on how long you held the investment and your total household income.

Is it better to withdraw from a brokerage account or an IRA first?

There’s no “one size fits all” approach, but many retirees benefit from using their taxable brokerage accounts first for income. It allows tax-deferred accounts more time to compound and can help you manage to stay below the thresholds for IRMAA surcharges or higher capital gains rates. In 2026, married couples can have a taxable income of up to $98,900 and still qualify for a 0% federal tax rate on their long-term gains.

About the Author

Joseph A. Eck, CFP®, is the owner and lead financial advisor at Stage Ready Financial Planning. With a background as a music educator and over a decade of experience as a financial planner, Joseph brings a teacher’s heart and a conductor’s precision to retirement planning and investing strategies. He is dedicated to helping families across Dayton and Southwestern Ohio achieve peace of mind by synchronizing their investments, taxes, and income goals into a single, high-performance retirement strategy.

Article References

- Kiplinger. “Medicare Premiums 2026: IRMAA Brackets and Surcharges for Parts B and D.” Accessed February 23, 2026. https://www.kiplinger.com/retirement/medicare/medicare-premiums-2026-irmaa-brackets-and-surcharges-for-parts-b-and-d

- T. Rowe Price. “How to make the most of your savings using a tax-efficient approach.” Accessed February 23, 2026. https://www.troweprice.com/personal-investing/resources/insights/how-to-make-most-of-your-savings-using-tax-effficient-approach.html

- Nasdaq. “The Fall of a Blue Chip: General Electric’s Horrible 2018.” Accessed February 23, 2026. https://www.nasdaq.com/articles/fall-blue-chip-general-electrics-horrible-2018-2018-12-10

- Morningstar. “How ETFs Help You Cut Your Tax Bill.” Accessed March 2, 2026. https://www.morningstar.com/funds/how-etfs-help-you-cut-your-tax-bill-2

- Internal Revenue Service. “Topic No. 559: Net Investment Income Tax.” Accessed March 2, 2026. https://www.irs.gov/taxtopics/tc559

- Vanguard. “Tax-Efficient Retirement Plan Strategies: Withdrawal Order.” Accessed March 2, 2026. https://investor.vanguard.com/advice/tax-efficient-retirement-strategy

- Charles Schwab. “Is Direct Indexing Right for You?” Accessed March 2, 2026. https://www.schwab.com/learn/story/is-direct-indexing-right-you

- Fidelity Investments. “3 Reasons to Stay Invested.” Accessed March 2, 2026. https://www.fidelity.com/learning-center/wealth-management-insights/3-reasons-to-stay-invested

This communication is for informational purposes only and is not intended as investment advice, tax advice, accounting, or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision. Past performance is no indication of future results.