Ever have the frustrating experience of finding out you’re paying more for something but you’re not getting any added benefit? My retired clients feel this way when they find out they have to pay Medicare IRMAA surcharges. These are Medicare premium increases that work like an added tax because your income was too high.

The good news is that IRMAA can be avoided and even appealed if you have a qualifying life-changing event (like retirement). If you’re wondering how to avoid IRMAA surcharges, you’ve found the right article. We’ll discuss how you can fine-tune your income and protect your retirement savings.

Key Takeaways

- IRMAA Two-Year Look Back: Your 2026 Medicare premiums are determined by the income you reported in 2024. You’ll need to plan proactively to avoid IRMAA.

- The IRMAA Cliff: Crossing an IRMAA threshold by just $1 triggers the full surcharge for the entire year.

- You Can Appeal: You might be able to reverse IRMAA surcharges if your income dropped due to a qualifying life event like retirement or work reduction.

What Is IRMAA and Why Does It Matter?

According to the Centers for Medicare & Medicaid Services, about 8% of Medicare beneficiaries pay an income-related monthly adjustment (IRMAA) surcharge. These extra premiums were originally introduced as part of the Medicare Modernization Act of 2003, taking effect for Medicare Part B in 2007 and expanding to Part D in 2011.

The Social Security Administration coordinates with the IRS each year to check your income from 2 years ago. If your modified adjusted gross income crosses certain limits, you’re hit with a related monthly adjustment amount. SSA data states that the government pays about 75% of the Part B premium for most retirees, but higher income medicare beneficiaries pay more. Instead of 25% of the cost of Medicare, they have to pay between 35% to 85% of the total thanks to IRMAA.

How IRMAA Thresholds Work (The Cliff Problem)

Medicare premium tax brackets use what’s referred to as a cliff system. If your modified adjusted gross income (MAGI) goes even $1 over a threshold, you’ll have to pay the higher associated premium for the entire year. For higher income Medicare beneficiaries, that extra dollar of income could cost thousands in premium surcharges.

The table below shows the 2026 thresholds and the surcharges apply to both spouses if you’re married and filing jointly.

2026 Medicare IRMAA Income Brackets

| If Your 2024 MAGI Was: (Individual) | If Your 2024 MAGI Was: (Joint) | Part B Monthly Surcharge | Part D Monthly Surcharge |

| $109,000 or less | $218,000 or less | $0.00 | $0.00 |

| $109,001 – $137,000 | $218,001 – $274,000 | +$81.20 | +$14.50 |

| $137,001 – $171,000 | $274,001 – $342,000 | +$202.90 | +$37.50 |

| $171,001 – $205,000 | $342,001 – $410,000 | +$324.60 | +$60.40 |

| $205,001 – $499,999 | $410,001 – $749,999 | +$446.30 | +$83.30 |

| $500,000 or more | $750,000 or more | +$487.00 | +$91.00 |

*https://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles

Example: In 2026, the base Medicare Part B premium is $202.90. Let’s say you and your spouse file jointly and are both over age 65, enrolled in Medicare Part B. If your MAGI in 2024 was $219,000, you’d each have to pay an additional $81.20 for Part B. This would increase your household Medicare premiums from $405.80 to $568.20.

What Income Counts Toward IRMAA?

Instead of using your taxable income or adjusted gross income, Medicare IRMAA surcharges apply based on your modified adjusted gross income (MAGI). To make things confusing, if you look up MAGI, you’ll find that there are a few different versions based on different tax situations.

For Medicare IRMAA, the MAGI math is pretty simple. You don’t have to worry about adding back IRA deductions, student loan interest, or tax credits. Your Medicare IRMAA MAGI is just two lines on your standard federal tax return.

To find your number, you’ll take your adjusted gross income, sitting on Line 11 of your Federal Form 1040, and add back your tax exempt interest from Line 2a. In some circumstances, the Social Security Administration also requires you to add back excluded foreign earned income if you lived overseas.

Your adjusted gross income on line 11 includes the following income sources:

- Wages from a part-time work or earned income

- The taxable portion of your Social Security benefits

- Payouts from pensions or pre-tax retirement accounts

- Capital gains from selling a stock, fund, or real estate

- Interest and dividends from your bank accounts and brokerage accounts

Line 2a tracks your municipal bond interest and distributions from tax-exempt bond funds.

What It Looks Like In Real Life

In 2024, Bob and Carol were retired and not drawing Social Security. They took out $180,000 from their traditional IRAs for income. This makes their adjusted gross income on Line 11, $180,000. They also own local municipal bonds that paid them $40,000 tax-free interest, located on line 2a.

When Medicare looks at their tax return for IRMAA in 2026, they’ll add those two lines together ($180,000 + $40,000). Their Medicare MAGI for 2024 would have been approximately $220,000, pushing them past the $218,000 threshold and into the first surcharge bracket.

8 Smart Ways to Avoid IRMAA Surcharges

1. Manage Your Retirement Withdrawals Strategically

If you use your traditional IRA or pre-tax 401(k) for income in retirement, every dollar you take out counts towards your MAGI. If you need extra cash for a new car or a vacation, it can easily push you right over an IRMAA cliff.

One of the easiest ways to manage or avoid IRMAA is to be strategic about the accounts you use for income in retirement. If you’re close to potential IRMAA brackets, you could reduce your MAGI by taking less out of your IRA or 401(k) and more from one of the following sources:

- Roth IRA or Roth 401(k): Qualified withdrawals are tax-free and don’t increase your AGI.

- Health Savings Accounts (HSAs): If used for qualified medical expenses, HSA distributions are entirely invisible to Medicare.

- The basis in your taxable accounts: When you sell an investment, you’re only taxed on the growth (the capital gain). The original money you put in (your basis) comes back to you tax-free and won’t affect your IRMAA calculation.

- Cash savings and High-Yield Savings Accounts (HYSAs): The interest your cash earns is taxable each year whether you use your cash or not. Taking income from cash accounts doesn’t increase your AGI.

Example: Dave and Sarah need $40,000 for an exciting home renovation project. If they pull the full $40,000 from Sarah’s traditional IRA, that amount increases their AGI and can push them right over an IRMAA cliff.

Instead, they orchestrated their withdrawal in a more tax-efficient way. They took $15,000 from her traditional IRA, $15,000 from her Roth IRA, and $10,000 from their high-yield savings account. They still pulled out $40,000, but they only reported $15,000 to the IRS and Medicare, dodging IRMAA.

2. Maximize Pre-Tax Retirement Contributions

If you or your spouse has earned income from a job, you might be able to use pre-tax retirement accounts to lower your MAGI. Contributions to your 401(k) or traditional IRA lower the income reported on Line 11 (AGI) of your tax return. This can be helpful starting around age 63 because of the Medicare IRMAA 2 year look back.

You can use this strategy even if only one of you has earned income. IRS spousal IRA rules allow a working spouse’s earned income to be used to fund a traditional IRA for a retired spouse. In 2026, savers age 50 or older can contribute up to $8,600 to a traditional IRA (subject to deduction limits). Maxing out both IRAs could lower your AGI by up to $17,200. You could deduct even more if you have a job with access to a 401(k).

Example: In 2024, Jim was fully retired, but his wife, Karen, earned $30,000 from a part-time job. Their total income was $225,000, putting them over the $218,000 IRMAA cliff for 2026. To lower their future Medicare costs, Karen uses her income to max out a traditional IRA for herself ($8,000) and a spousal traditional IRA for Jim ($8,000). These contributions drop their joint Line 11 AGI to $209,000, putting them under the first IRMAA cliff.

3. Reduce Future Required Minimum Distributions (RMDs)

When you put money into a traditional IRA or pre-tax 401(k), you get a tax deduction, but eventually you’ll pay tax on it. At age 73 or 75, the IRS makes you take yearly mandatory withdrawals called Required Minimum Distributions (RMDs). And your RMDs count towards your AGI and MAGI for Medicare IRMAA, unless you donate them directly to a charity (More on this shortly).

But you don’t have to wait for RMDs to drive up your tax bill and Medicare premiums. The IRS determines your RMD based on the total balance of your pre-tax accounts. The lower those balances are, the lower your future forced withdrawals will be. You can strategically trim these balances by:

- Taking earlier withdrawals from your pre-tax accounts

- Starting Roth conversions (Moving money from your IRAs to Roth IRAs and paying the tax up front)

- Using Qualified Charitable Distributions (QCDs)

For more information on how these concepts work and about lowering the tax impact of RMDs, check out my recent blog article: How Can Retirees Minimize RMD Taxes? 5 Strategies for You to Consider

Example: Robert is 62 and he has a large traditional IRA that might eventually force him to take $80,000/yr in RMDs at age 73. He’s worried about navigating Medicare IRMAA when that happens, so he doesn’t let that balance sit and grow. Instead, he starts taking smaller, strategic withdrawals right now to live on now that he’s retired. He also works with his financial advisor and tax professional to start a Roth conversion strategy. By lowering his overall pre-tax balance today, he scales back his future mandatory distributions, potentially keeping his income under the IRMAA surcharge brackets.

4. Plan Roth Conversions Carefully

A Roth conversion is when you move money from a traditional, pre-tax retirement account into a Roth IRA. You pay taxes on the conversion amount, and then those dollars can grow tax-free for the rest of your life.

You can use Roth conversions to lower RMDs, but you have to be careful. Because the IRS treats your conversion as taxable income, you’ll increase your AGI. If you move too much money in any one year, you might trigger IRMAA surcharges down the road, defeating the purpose of using Roth conversions to manage RMDs.

When I work with my clients on Roth conversions, usually we’ll partner with their tax professional to figure out how much we can convert without potentially triggering Medicare IRMAA. We work to convert amounts below the cliff brackets unless the client or their tax professional says otherwise.

If you want to learn more about Roth conversions and when they’re helpful, check out my recent blog article: What Is a Roth Conversion & Is It Right for You? In-Depth Guide

Example: In 2024, Mark and Linda were 63 and they wanted to convert some of their traditional IRA money to Roth. Their AGI was around $150,000. Because the official numbers aren’t released in advance, they worked with their financial advisor and CPA to estimate the future thresholds, targeting a safe limit of $218,000. Instead of converting a massive lump sum, they converted only $60,000. They increased their tax-free Roth savings while successfully keeping their total MAGI under the actual surcharge bracket for 2026.

5. Use Qualified Charitable Distributions (QCDs)

Earlier I mentioned that you could reduce the tax impact of RMDs by giving to a charity. The way you do this is by completing a Qualified Charitable Distribution (QCD). It’s a pretty powerful tax-saving instrument, especially if you’re worried about Medicare IRMAA.

You execute a QCD by sending money directly from your traditional IRA to a qualified 501(c)(3) charity. The funds never pass through your personal bank account, so the IRS doesn’t count the distribution towards your AGI and MAGI. At the same time, according to IRS Publication 590-B, the QCD satisfies your RMD for the year.

To use this strategy, you’ll need to follow a few rules:

- You must be 70.5 or older

- The QCD check must go directly from your IRA to the charity

- 501(c)(3) status is required for the charity to count

- The 2026 annual limit is $111,000 per person ($222,000 for married couples if both have their own IRAs).

- It can’t go to a Donor-Advised Fund (DAF)

Example: Susan is single and at age 74 had an RMD of $30,000 in 2024. She supports her local animal shelter and gives them $10,000 a year. Her base AGI was around $85,000. If Susan took her full RMD as income, her total 2024 AGI would have been $115,000, pushing her over the $109,000 threshold for IRMAA surcharges in 2026.

Instead, Susan executed a QCD. She had her IRA custodian send $10,000 directly to the shelter and took the remaining $20,000 as income. She satisfied her $30,000 RMD, but only reported $20,000 of income to the IRS. Her final AGI landed at $105,000, keeping her under the first IRMAA threshold.

6. Use Tax-Loss Harvesting to Lower Your Capital Gains

If you have a brokerage account, you can use investment losses to lower your year-end income. You can’t modify your pension or Social Security, but you can choose to sell an underperforming investment to offset capital gains, otherwise known as tax-loss harvesting.

The IRS lets you use realized losses to wipe out your capital gains, and if your losses are greater than your gains, you can use up to $3,000 of the extra loss to reduce your ordinary income for the year. Tax-loss harvesting is an advanced strategy and you should definitely work with your tax advisor and financial planner to handle issues like:

- The wash-sale rule: If you sell an investment for a tax loss, you can’t buy the same investment back within 30 days after the sale. Doing so disallows your tax loss. According to a helpful article by Vanguard, you can swap the sold investment with a similar but different asset to avoid this issue.

- Carryover losses: If your net capital loss exceeds the $3,000 limit, you don’t lose it. The IRS lets you carry extra losses forward to offset your capital gains in future tax years.

Example: David is single and fully retired. After reviewing his expected 2026 income with his advisor he realized that his estimated AGI would be close to $111,000. This could put him in the zone of having IRMAA surcharges for 2028. So David looks at his taxable account, and sells an underperforming fund with an $8,000 loss. It wipes out his current capital gains and hopefully drops his final 2026 AGI down to around $103,000, keeping him further away from dealing with IRMAA.

7. Avoid One-Time Income Spikes when Possible

Tax-loss harvesting is great for simple year-end planning, but it probably won’t save you from a big tax event, like a business or real estate sale. If you want to avoid triggering IRMAA during these situations, you should work with your financial planner and tax professional and consider strategies like:

- Spreading out your investment sales: You could break up taxable account rebalancing into multiple years to keep your annual capital gains low.

- Time your real estate sales with low-income years: If you need to sell an investment property that’s appreciated, you could wait for a low-income year, or well before you enter Medicare at age 65, to avoid IRMAA issues.

- Bundle deductions to offset business sales: Time large charitable donations or deductible medical expenses to hit in the same tax year as a business exit to offset the income spike.

- Take installments carefully: If you own a business, you might be able to use an installment agreement to defer income over multiple years.

Example: Mark and Linda decided to sell an appreciated rental property. If they closed the sale during a normal income year, the extra capital gains would bump up their AGI and force them to deal with IRMAA surcharges. To protect their budget, they timed the sale to close right after they both retired but before their pension and Social Security benefits kicked in.

8. Consider Appealing IRMAA if Your Income Drops

If you get an IRMAA surcharge notice in the mail, the good news is that you may be able to reverse it. Medicare looks back two years, so your current premiums might be based on your high-earning years, even if you’re making less money now. If your income dropped because of a qualifying life transition, you can ask the Social Security Administration (SSA) to remove the surcharges.

What events can I appeal?

There are eight qualifying life-changing events recognized by the SSA where IRMAA can be successfully appealed. The big ones include involuntary or permanent life shifts like retirement (work stoppage), a major reduction in work hours, divorce, or the death of your spouse.

What events can’t I appeal?

You probably won’t succeed at appealing a voluntary investment or financial choice. Things like taking a large distribution from an inherited IRA, selling a primary home or rental property, or a big Roth conversion would not count. The SSA views these as voluntary spikes, not life-changing hardships.

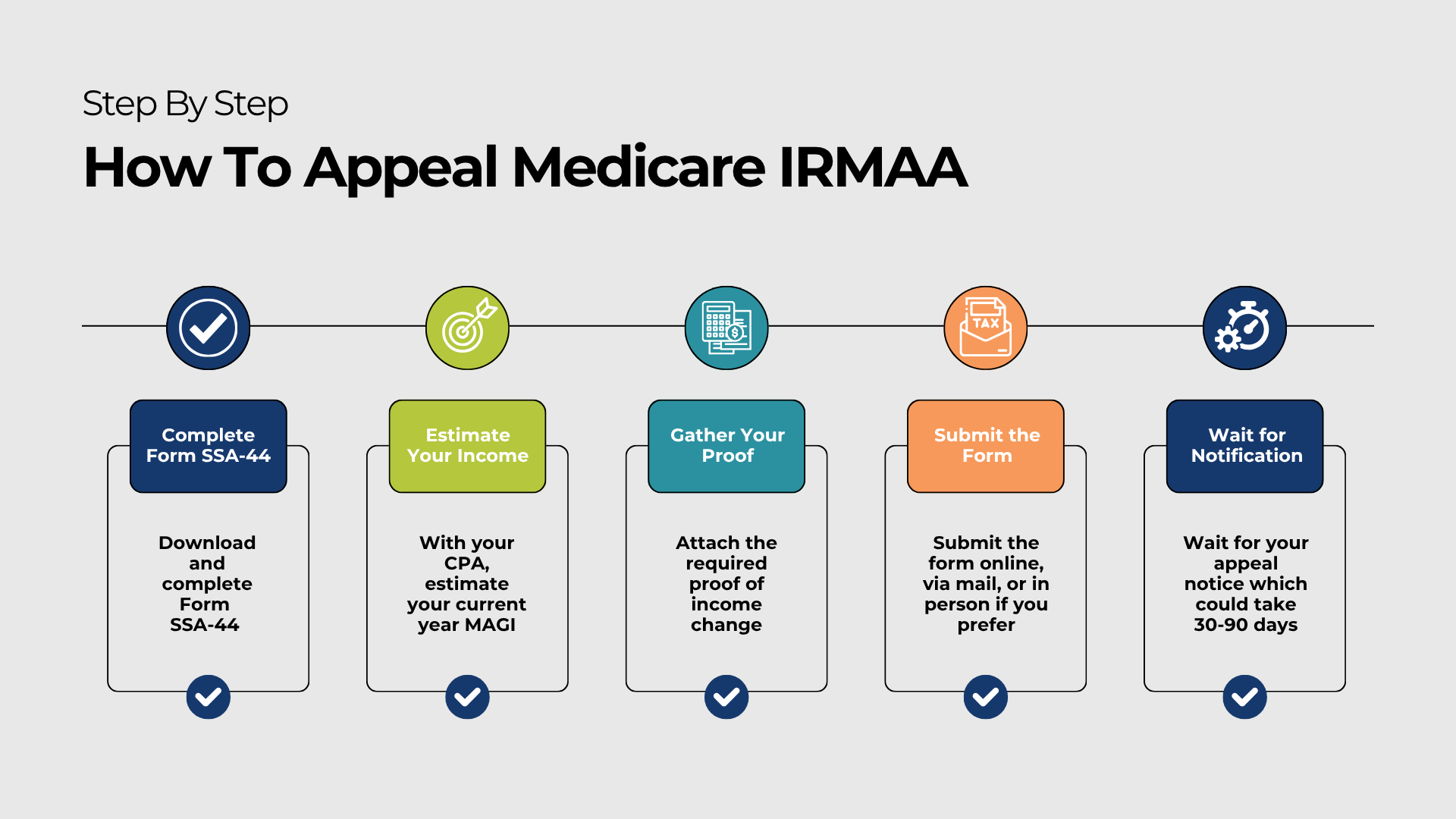

If you’ve had a qualifying event, you can navigate the appeal process by following these steps:

- Complete Form SSA-44: Download and complete a copy of Form SSA-44 (Medicare IRMAA – Life-Changing Event).

- Estimate your income: Work with your tax professional to fill out the form and enter a realistic estimate of your current year modified adjusted gross income (MAGI).

- Gather your proof: Attach documentation proving both the event and your income drop. If you retired, this could include a formal termination letter from your employer or your final pay stubs.

- Submit the form: According to the Social Security Administration, you upload your completed form securely through your account on SSA.gov. You can also mail it or drop it off at your local Social Security office.

- Wait for notification: Hearing back can take between 30 to 90 days. The SSA will mail a physical Notice of Reconsideration letter to your home once a decision is reached.

Example: Tom retired at the end of 2024, and his income dropped in 2025. In 2026 his Medicare bill arrived showing IRMAA surcharges because the government used his 2024 tax return. Tom uploaded Form SSA-44 to his online Social Security account, citing his retirement as the qualifying event for appealing IRMAA. He included his formal retirement letter and an estimate of his lower 2025 income with the help of his CPA. A few weeks later, he got his approval notice in the mail. The SSA wiped out his 2026 surcharges and issued a retroactive refund credit for the higher premiums he’d already paid.

Common IRMAA Mistakes to Avoid

We’ve covered a lot of these so far, but here are some common IRMAA mistakes you can easily avoid:

| Common Mistake | Why it’s an Issue |

| Forgetting about tax-free interest | Many retirees think municipal bond interest is safe because it’s federally tax-free. But the SSA adds tax-exempt interest right back into your MAGI calculation for IRMAA purposes. |

| Failing to plan ahead | If you wait until age 65 to plan your income, it might be too late. Because of Medicare’s look-back rule, financial decisions you made at age 63 determine your initial Medicare premiums. |

| Thinking any income drop can be appealed | Sadly, you can’t always appeal IRMAA surcharges. The SSA rejects appeals for things like stock sales, home downsizes, or Roth conversions. |

| Treating IRMAA brackets like normal tax brackets | Standard income brackets are progressive, but IRMAA brackets work on a cliff system. Crossing a bracket by just one dollar triggers the full surcharge for that year. |

Want More Retirement Planning Help? Contact Stage Ready for a Complimentary, No-Commitment Consultation

If you want to avoid or minimize Medicare IRMAA, you’ll need to monitor it every year. This means careful planning when it comes to how you spend your retirement savings.

Stage Ready Financial Planning was built to help families in Dayton and Southwest Ohio fine-tune their retirement distribution strategies as tax-efficiently as possible. I work directly with you to navigate the shifting tax rules, handle the math, and make sure you’re keeping as much of your retirement income as possible instead of overpaying for Medicare.

If you’ve saved $750,000 or more for retirement and want to make sure your wealth management plan is working in sync, let’s talk. Schedule your complimentary intro call today!

Frequently Asked Questions (FAQs)

What income triggers IRMAA surcharges?

The Social Security Administration looks at your modified adjusted gross income (MAGI) to figure out if you have to pay IRMAA. They calculate your MAGI by taking your adjusted gross income on line 11 of your federal 1040 and adding in line 2a for tax exempt interest from things like municipal bond funds. In 2026, the MAGI amounts that trigger IRMAA are $109,000 for single filers and $218,000 for married couples filing jointly.

How do I avoid IRMAA in 2026?

Medicare IRMAA is issued on a two-year look-back, so your income in 2024 determines your 2026 premiums. If you want to avoid surcharges, you’ll need to have kept your income low enough 2 years ago or you’ll need to file an appeal in 2026 if you had a qualifying life event after 2024.

Are Roth IRA withdrawals counted toward IRMAA?

I’m happy to say no. Qualified Roth IRA withdrawals don’t count towards your modified adjusted gross income. If you have a Roth IRA, it’s a great place to draw extra income if you’re worried about avoiding IRMAA surcharges..

Can IRMAA be appealed?

Yes. If your income dropped because of a qualifying and involuntary life event like a complete retirement (work stoppage) or a major reduction in work hours, you can ask the Social Security Administration to remove the surcharges. If you want to do this, you’ll need to download Form SSA-44, provide a signed estimate of your current year income, attach supporting proof like a termination letter, and submit it through your account on SSA.gov. The SSA recognizes eight qualifying life events, including retirement, divorce, marriage, or the death of a spouse.

Is IRMAA permanent?

It depends on what caused your income to go up. IRMAA isn’t permanent for life, because the SSA recalculates your premiums every year based on your next tax return. If your premium spike was because of a voluntary financial choice like a large Roth conversion or a stock sale, you can’t appeal it, and you’re stuck paying that higher premium for the calendar year. Your premiums will go back down once the next tax return they review falls below your current thresholds.

About the Author

Joseph A. Eck, CFP®, is the owner and lead financial advisor at Stage Ready Financial Planning in Dayton, Ohio. He specializes in helping retirees synchronize their tax strategies and investment goals to minimize unnecessary costs like IRMAA surcharges. With a background in education and over a decade in personal finance, Joseph brings a teacher’s heart and a conductor’s discipline to financial planning, helping clients find the right rhythm for their retirement income. Learn more about Joe.

About Stage Ready Financial Planning

Stage Ready Financial Planning provides wealth management and fee-only financial planning designed specifically for retirees and savers over age 50 in Dayton and Southwest Ohio. If you’ve saved $750,000 or more for retirement, Joseph Eck, CFP® helps you filter out the “noise” of market volatility and complicated tax rules so you can focus on the life you’ve worked so hard to build.

Instead of spending your time worrying about the market, you’ll get a living, breathing plan, built step-by-step, that stays in sync with your ideal lifestyle. Stage Ready Financial Planning specializes in helping you orchestrate a predictable retirement paycheck, professionally managing your portfolio for lasting income, and proactively reducing the “IRS’s cut” of your savings.

Article References

- Centers for Medicare & Medicaid Services (CMS). “2026 Medicare Parts A & B Premiums and Deductibles.” Accessed May 11, 2026. https://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles

- SSA.gov. “Benefits Planner: Retirement | Medicare Premiums.” Accessed May 11, 2026. https://www.ssa.gov/benefits/medicare/medicare-premiums.html

- Congress.gov. “H.R.1 – Medicare Prescription Drug, Improvement, and Modernization Act of 2003.” Accessed May 11, 2026. https://www.congress.gov/bill/108th-congress/house-bill/1

- Social Security Administration. “POMS: HI 01101.010 – Modified Adjusted Gross Income (MAGI).” Accessed May 18, 2026. https://secure.ssa.gov/poms.nsf/lnx/0601101010

- Internal Revenue Service. “Publication 590-A: Contributions to Individual Retirement Arrangements (IRAs).” Accessed May 18, 2026. https://www.irs.gov/publications/p590a

- Internal Revenue Service. “Publication 590-B: Distributions from Individual Retirement Arrangements (IRAs).” Accessed May 18, 2026. https://www.irs.gov/publications/p590b

- Charles Schwab & Co. “Reducing RMDs with QCDs.” Accessed May 18, 2026. https://www.schwab.com/learn/story/reducing-rmds-with-qcds

- Vanguard. “Maximize your tax savings with tax-loss harvesting” Accessed May 18, 2026. https://investor.vanguard.com/investor-resources-education/taxes/offset-gains-loss-harvesting#:~:text=to%20process%20transactions.-,Wash%2Dsale%20rule,the%20loss%20will%20be%20disallowed.

- Social Security Administration. “Request to lower an Income-Related Monthly Adjustment Amount (IRMAA).” Accessed May 18, 2026. https://www.ssa.gov/medicare/lower-irmaa

- Social Security Administration. “Medicare Income-Related Monthly Adjustment Amount – Life-Changing Event (Form SSA-44).” https://www.ssa.gov/forms/ssa-44.pdf

This communication is for informational purposes only and is not intended as investment, tax, accounting, or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision. Past performance is no indication of future results.